Agility in Acquisition: How Reverse 1031 Exchanges Secure the Perfect Deal

📌 Key Takeaways

A reverse 1031 exchange lets you buy the replacement property first—before selling your current one—while still deferring capital gains taxes.

Structure Before You Close: You must set up the exchange arrangement before buying the new property—closing in your own name first kills the tax deferral completely.

Someone Else Holds the Title: A special entity called an Exchange Accommodation Titleholder (EAT) temporarily owns the new property until your old one sells, keeping you compliant with IRS rules.

Same Deadlines Still Apply: You have 45 days to formally identify which property you're selling and 180 days total to complete the entire exchange—no extensions.

Costs More, But Math Often Works: Reverse exchanges add $15,000–$25,000 in fees, but that's small compared to potentially losing $200,000+ in tax savings or missing your ideal property.

Common Failures Are Preventable: Most reverse exchanges fail because investors buy first and ask questions later, or forget to submit required paperwork on time.

Lock in your next property without losing your tax deferral—but only if you build the structure before you buy.

Commercial real estate investors facing time-sensitive acquisition opportunities will find the compliance roadmap they need here, preparing them for the detailed process overview that follows.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

The call comes at 4:47 PM.

Your broker found it—the 48-unit multifamily two blocks from the new transit hub. The seller wants a decision by Friday. Your current property hasn't even hit the market yet. The spreadsheet on your desk shows $287,000 in potential capital gains tax if you buy wrong. The calendar shows 72 hours until someone else writes the offer.

You've spent years building equity in your Houston portfolio. Losing this deal because of timing feels wrong. Buying it incorrectly and destroying your tax deferral feels worse.

This is the exact moment a reverse 1031 exchange exists to solve. When the perfect replacement property appears before your sale closes, you don't have to choose between losing the deal and losing your tax deferral. A reverse exchange lets you acquire first—legally, compliantly, and with your equity fully protected.

A reverse 1031 exchange is a parking arrangement where an Exchange Accommodation Titleholder (EAT) holds the new property until the old one sells. Think of it like a bridge loan for ownership title—holding the new asset in a safe harbor until you're ready to dock. This structure exists specifically for property owners who find themselves on the right side of a timing problem: the replacement is ready before the relinquishment is complete.

The catch? Structure matters more than speed. Buying the property first without proper arrangements doesn't create a reverse exchange—it disqualifies your exchange entirely. The difference between preserving $287,000 in equity and writing a check to the IRS comes down to how the transaction is built before you close.

Why "Sell-Then-Buy" Breaks Real Deals for Active Property Owners

The conventional 1031 sequence makes sense on paper. Sell your relinquished property, identify replacements within 45 days, close on your new asset within 180 days. Clean. Linear. Predictable.

Real estate markets don't work that way.

In Houston's competitive acquisition environment, quality assets move fast. A well-located multifamily with value-add potential doesn't wait for your sale to close. Neither does the industrial property near the port expansion or the retail center with below-market rents. By the time your relinquished property sells, the replacement you wanted has three backup offers.

The sell-then-buy model creates four specific problems for active property owners:

Deal flow disruption. Your acquisition timeline becomes hostage to your disposition timeline. If your buyer's financing falls through, your replacement property is gone.

Lost purchase leverage. Sellers prefer clean offers with certain funding. "I'll buy this once I sell my other property" is a weaker position than "I'm ready to close."

Forced compromise. When your 45-day identification clock is ticking and your first-choice property sold to someone else, you settle for the second or third option. That compromise compounds over decades of ownership.

Fire-sale pressure. Knowing you need to sell fast to catch a replacement opportunity, buyers negotiate harder on your relinquished property. You lose equity on both ends.

The standard sequence assumes the market will cooperate with your timeline. For individual investors pursuing specific opportunities, that assumption costs real money.

What a Reverse 1031 Exchange Is (And What It Isn't)

A reverse 1031 exchange flips the standard sequence: you acquire the replacement property first, then sell the relinquished property second—all while maintaining full tax deferral under Internal Revenue Code Section 1031.

The IRS established a safe harbor for reverse exchanges under Revenue Procedure 2000-37, later modified by Revenue Procedure 2004-51. These procedures define exactly how the structure must work to qualify for safe harbor treatment.

Here's what a reverse exchange is not: a paperwork fix after the fact.

If you close on a replacement property in your own name before engaging a qualified intermediary and establishing proper structure, you don't have a reverse exchange. You have a taxable purchase followed by a taxable sale. The sequence cannot be reconstructed retroactively.

The critical difference is ownership. In a standard forward exchange, you never take possession of the sale proceeds—your QI holds them. In a reverse exchange, you cannot take ownership of the replacement property directly. An Exchange Accommodation Titleholder must hold title to prevent you from owning both properties simultaneously.

This requirement isn't a technicality. It's the foundation of compliance. The IRS requires that the exchanger never hold title to both the relinquished and replacement properties at the same time. The EAT exists to maintain that separation.

The EAT Explained: Exchange Accommodation Titleholder

The Exchange Accommodation Titleholder is the entity that makes reverse exchanges possible. Understanding its role removes most of the complexity.

An EAT is a special-purpose entity, typically established by your qualified intermediary, that temporarily holds title to either the replacement property (in most cases) or the relinquished property. The EAT is not your company. It's not your LLC. It's an independent entity specifically created to "park" property during the exchange period as part of a Qualified Exchange Accommodation Arrangement (QEAA).

What the EAT does:

The EAT takes legal title to the replacement property at closing. It holds that title while you complete the sale of your relinquished property. Once the exchange is complete, the EAT transfers title to you. Throughout this process, the EAT maintains the separation required by IRS rules.

Why the EAT must hold title:

Without the EAT, you would own both properties simultaneously the moment you close on the replacement. That simultaneous ownership violates the fundamental requirement of a 1031 exchange—that you're exchanging one property for another, not accumulating both.

The EAT prevents what the IRS calls "constructive receipt." Just as your QI holds funds in a forward exchange to prevent you from touching the money, the EAT holds title in a reverse exchange to prevent you from holding both assets. Constructive receipt disqualifies the exchange—even if you never intended to keep both properties.

The mechanism of failure this prevents:

Many property owners assume they can buy the replacement property directly, then "fix the paperwork" by engaging a QI and completing a 1031 on the sale of their old property. This approach fails completely. Once you own the replacement in your own name, the exchange is disqualified before your relinquished property even hits the market. The EAT structure must be in place before you acquire.

Reverse Exchange Workflow: Title and Funds in Plain English

The reverse exchange process involves more parties and more steps than a standard forward exchange. Here's how title and funds actually move:

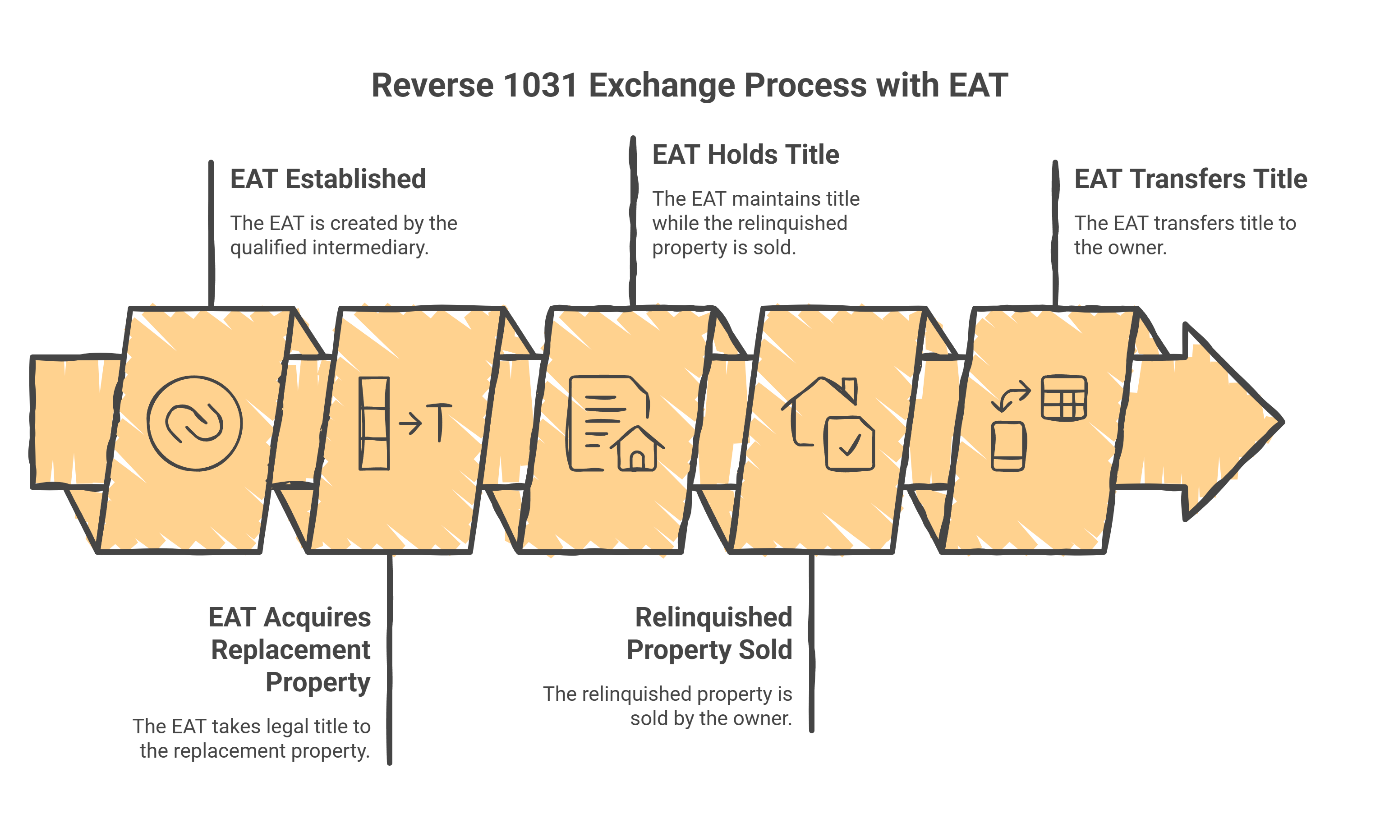

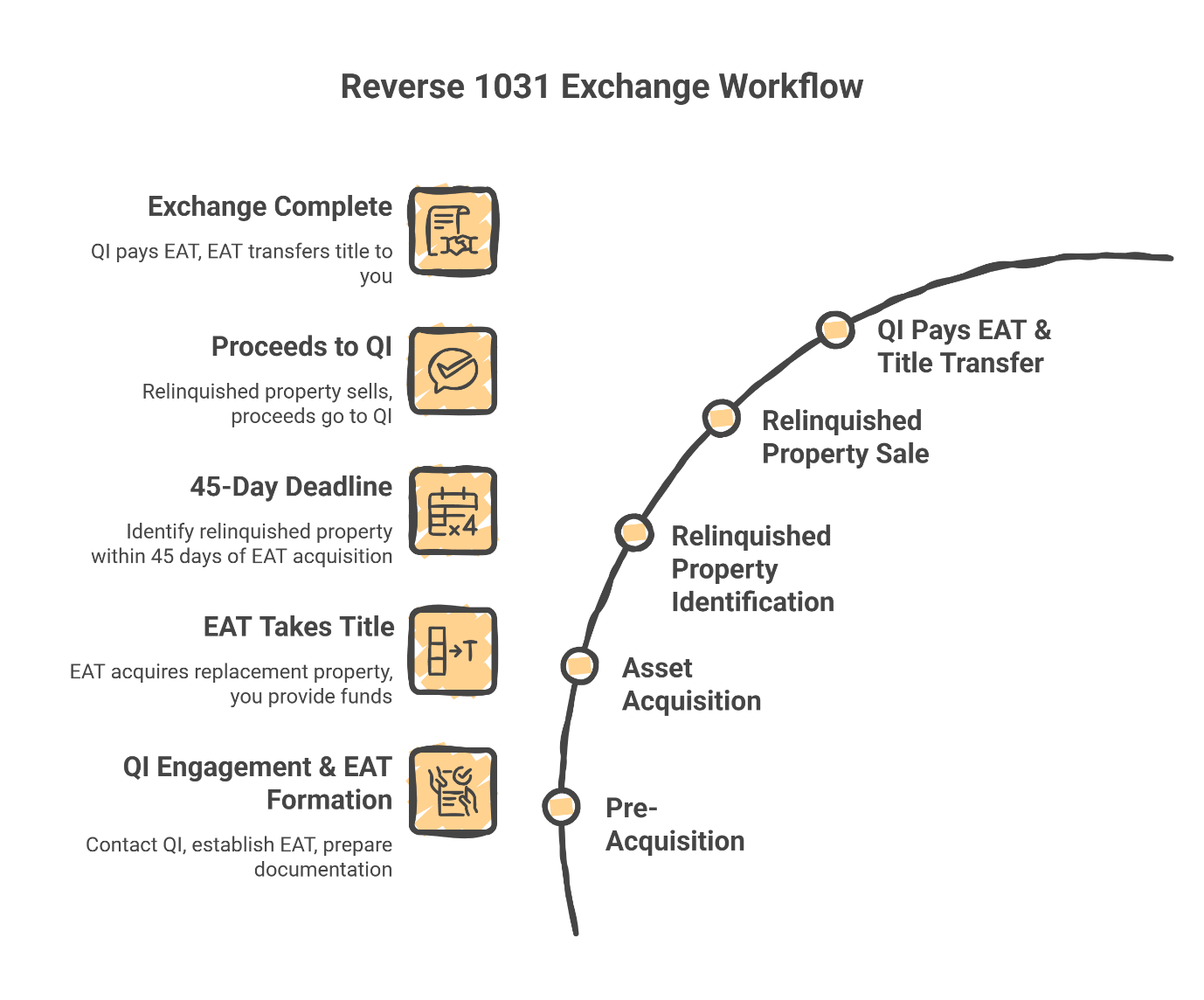

Step 1: Pre-Acquisition Phase: QI Engagement and EAT Formation

Before you sign the purchase agreement on the replacement property, contact an attorney-led qualified intermediary. The QI will establish the Exchange Accommodation Titleholder entity and prepare the exchange documentation. This step is non-negotiable timing—structure must exist before acquisition.

Step 2: Asset Acquisition and Title Parking

At closing, the EAT takes title to your replacement property. You provide the funds for the purchase (typically through a loan to the EAT or direct funding), but the EAT appears on the deed as the owner. The EAT and you enter into a Qualified Exchange Accommodation Agreement (QEAA) that governs the parking arrangement.

Step 3: You Market and Sell Your Relinquished Property

With the replacement safely parked, you proceed to sell your relinquished property. The 45-day identification deadline applies here—but in reverse. You must identify which property you will sell (your relinquished property) within 45 days of the EAT's acquisition of the replacement.

Step 4: Disposition and Liquidity Capture

When your relinquished property sells, the proceeds go to your qualified intermediary, just like a standard forward exchange. The QI holds these funds.

Step 5: QI Pays the EAT; EAT Transfers Title to You

The QI uses the exchange funds to "purchase" the replacement property from the EAT. The EAT transfers title to you. The exchange is complete.

The QI facilitates the exchange and holds funds. The title company handles closings. The EAT holds title during the parking period. Each party has a distinct role that maintains IRS compliance.

Reverse Exchange Deadlines: The 45-Day and 180-Day Clock Still Applies

The timing rules for reverse exchanges mirror forward exchanges—but the identification requirement works differently.

The 45-Day Identification Deadline

In a reverse exchange, you must identify which property you will sell (your relinquished property) within 45 days of the EAT acquiring the replacement property. This identification must be in writing and delivered to your QI.

Most reverse exchangers already know which property they're selling—that's why they're doing a reverse exchange. The 45-day rule still requires formal written identification.

The 180-Day Completion Deadline

The entire exchange must be completed within 180 days of the EAT's acquisition. This means your relinquished property must sell and the title transfer from EAT to you must occur within that window.

No Extensions. No Exceptions.

Strict Statutory Deadlines. These deadlines are statutory, and the IRS provides virtually no extensions for reverse exchanges, with the rare exception of Presidentially declared disaster areas or specific military service extensions under IRC Section 7508. Weekends and holidays count toward your total; if Day 180 falls on a Sunday, you do not receive an extension to Monday. A common misconception is that the identification period and exchange period stack sequentially—they don't. The 180-day window runs from Day 0, with the 45-day identification deadline falling within it, not added to it.

The IRS requires reporting completed exchanges on Form 8824, which means your documentation must support every deadline and transfer throughout the process.

Practical Timeline Planning:

Day 0 marks when the EAT acquires the replacement property. Between Day 1 and Day 45, you must identify your relinquished property in writing. Between Day 1 and Day 180, you must sell your relinquished property and complete the title transfer from the EAT.

For Houston-area property owners, this timeline means your relinquished property should be market-ready before you acquire the replacement. Having a listing agreement in place, or better yet an accepted offer, reduces the risk of missing the 180-day deadline.

Cost vs. ROI: Why a Reverse Exchange Is Often Worth It

Reverse exchanges cost more than forward exchanges. The EAT structure requires additional legal documentation, the parking arrangement involves holding costs, and the QI's work is more complex.

For many property owners, the math still favors the reverse exchange by a wide margin.

The Real Comparison:

Consider an investor selling a $2.8 million Houston asset with approximately $1.15 million in capital gains. Between the 20% top-tier federal capital gains rate, the 3.8% Net Investment Income Tax (NIIT), and depreciation recapture (typically taxed at 25%), the potential tax liability reaches the $287,000 figure noted earlier. Depending on your specific tax bracket and the duration of your hold, these combined factors—along with potential state-level taxes—often result in an effective tax rate significantly higher than the federal base. You can estimate your own exposure using a 1031 exchange calculator before engaging your tax advisor for precise numbers.

A reverse exchange might add $15,000-$25,000 in fees and holding costs compared to a forward exchange. That's roughly 10% of the tax liability preserved.

But the calculation doesn't stop there.

Opportunity Cost of the Alternative:

If you wait to sell before acquiring, and the replacement property sells to another buyer, what's the cost? You might find another property—but it might be $100,000 more expensive, or in a less desirable location, or require more renovation. That "miss" compounds over your entire holding period.

The Decision Framework:

Document the specific replacement property opportunity. Calculate the tax deferral at stake. Add the opportunity cost of missing the acquisition. Compare against the incremental cost of reverse exchange structure. Factor compliance risk: a failed exchange costs 100% of the tax; a successful reverse exchange costs the fee differential.

A Fit-for-Purpose Tool:

Rather than treating reverse exchanges as "advanced-only," the better frame is fit-for-purpose. A reverse exchange matches situations where acquisition timing is the dominant risk—when the replacement is scarce, the sale is likely but not closed, and the cost of missing the deal exceeds the cost of structuring the transaction correctly.

Common Failure Points (And How Attorney-Led Structuring Reduces Risk)

Reverse exchanges fail for predictable reasons. Knowing these failure points helps you avoid them.

Failure Point 1: Premature Closing and Structural Absence

The most common failure. A property owner finds a property, gets excited, closes in their own name, then calls a QI asking how to "make it a 1031." By then, it's too late. The exchange was disqualified the moment they took title.

Prevention: Engage your QI before signing the purchase agreement on the replacement property.

Failure Point 2: Documentation Lapses and the Identification Window

Even though most reverse exchangers know exactly which property they're selling, they forget the formal written identification requirement. Day 46 arrives without proper documentation, and the exchange fails.

Prevention: Calendar the deadline. Prepare the identification letter immediately. Submit it early.

Failure Point 3: Relinquished Property Doesn't Sell in Time

The replacement is parked with the EAT, but the relinquished property sits on the market. Day 180 arrives with no buyer. The exchange fails, and the property owner may face tax consequences on both transactions.

Prevention: Have your relinquished property sale-ready before acquiring the replacement. Ideally, have an accepted offer or at minimum a listing agreement with realistic pricing.

Failure Point 4: QI Cannot Support EAT Structure

Not all qualified intermediaries can facilitate reverse exchanges. Some lack the legal infrastructure to establish and manage an EAT. If you engage a QI that only handles forward exchanges, you'll discover the limitation too late.

Prevention: Confirm EAT capability before engagement. Ask specifically about reverse exchange experience and legal structure.

Failure Point 5: Lender and Title Coordination Failures

Reverse exchanges require coordination between multiple parties. If your lender doesn't understand EAT structures, or if the title company has never closed a reverse exchange, delays can push you past deadlines.

Prevention: Work with professionals who have completed reverse exchanges. Your QI's team should include experienced attorneys who can coordinate with your lender and title company.

Reverse Exchange Readiness Checklist

Use this checklist to evaluate whether a reverse exchange fits your situation and what to prepare before engaging a QI.

When Reverse Exchange Makes Sense

You've identified a specific replacement property you want to acquire. The replacement is available now, but your relinquished property isn't sold. The tax deferral at stake exceeds $50,000. You have financing or capital available for the replacement acquisition. Your relinquished property is marketable within 180 days.

Pre-Closing Requirements

Engage an attorney-led qualified intermediary before signing the purchase agreement. Confirm the QI has EAT capability and reverse exchange experience. Establish the QEAA (Qualified Exchange Accommodation Agreement). Coordinate with your lender on EAT title holding requirements. Brief the title company on reverse exchange closing procedures.

What to Prepare Before Calling a QI

Replacement property details including address, purchase price, and closing timeline. Relinquished property details including address, estimated value, and current status. Estimated capital gain and tax liability. Financing plan for replacement acquisition. Realistic timeline for selling the relinquished property.

What Not to Do

Do not close on the replacement property in your own name. Do not assume paperwork can be fixed after acquisition. Do not engage a QI that lacks reverse exchange capability. Do not wait until your sale falls through to explore reverse options. Do not underestimate the 180-day deadline—calendar it immediately.

Your Next Move: Before the Deadline, Not After

The property owner who secures the 48-unit multifamily doesn't have better luck than the one who misses it. They have better structure.

If you're inside a contract window on a replacement property—or if you're actively pursuing specific assets while your current holdings haven't sold—time is your primary risk. Every day without proper structure in place is a day closer to either losing the deal or losing your tax deferral.

The reverse exchange process requires advance preparation. EAT establishment, QEAA documentation, lender coordination, and title company briefing all take time. Starting that process after you've found the perfect property means starting late.

Schedule a Consultation

Securitas 1031 provides attorney-led qualified intermediary services for Houston-area property owners and investors. Our team includes attorneys with tax law credentials who structure reverse exchanges, construction exchanges, and complex parking arrangements.

Before you sign your next purchase agreement, schedule a consultation to evaluate whether a reverse exchange protects your equity and secures your acquisition.

For brokers and advisors supporting clients through 1031 transactions, Securitas 1031 offers continuing education resources covering timing, rules, and key concepts.

Securitas 1031 440 Louisiana St Suite 1100, Houston, TX 77002 713-275-8112

Disclaimer: This article is for general informational purposes only and is not tax or legal advice. 1031 exchange requirements are fact-specific and can change. Consult your tax advisor and legal counsel before acting.

Disclaimer: This content is for informational purposes only and does not constitute legal, tax, or financial advice. 1031 exchange rules are highly technical and outcomes depend on your specific facts (including property descriptions, identification method, delivery/receipt process, and transaction timelines). Consult your qualified tax advisor and legal counsel before taking action.

Our Editorial Process:

Our expert team uses AI tools to help organize and structure initial drafts, conduct research, and refine content. Every AI-assisted draft is reviewed, edited, and verified by our human team to ensure accuracy, clarity, and practical value.

By: The Securitas 1031 Insights Team

The Securitas 1031 Insights Team is made up of seasoned, Houston-based legal and tax professionals who specialize in 1031 exchanges and real estate wealth strategy. We work with investors, business owners, and real estate professionals to simplify complex exchange rules and provide clear, actionable guidance. Our content is created for informational purposes and should not replace professional advice. Always consult your CPA, attorney, or qualified intermediary before taking action on a 1031 exchange.