The Failure of 'Commodity' QIs: Using Attorney-Led Compliance to Secure Your Exchange

📌 Key Takeaways

Choosing your Qualified Intermediary based on price alone can cost you up to 40% of your property gains in taxes.

"Fast and Cheap" Creates Real Risk: Budget QIs often lack the fund controls and legal structure needed for complex deals like reverse or improvement exchanges.

Constructive Receipt Kills Exchanges: If sale money touches your account—even briefly—the IRS treats it as income, and your tax deferral disappears completely.

Fund Safety Varies Wildly: Some QIs keep your money in separate accounts; others mix it with other clients' funds, leaving you exposed if the QI has financial trouble.

Ask Ten Questions Before Signing: Request written answers about fund handling, signatory controls, insurance coverage, and backup plans—vague responses signal weak protections.

Engage Your QI Before Closing: The safe harbor rules only protect you if the QI agreement exists before proceeds change hands, not the day of closing.

The right QI protects your equity; the wrong one hands it to the IRS.

Commercial property investors running exchanges with tight timelines or complex structures will find critical vetting criteria here, preparing them for the detailed compliance requirements that follow.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

The closing is in nine days. Your buyer's wire is confirmed. And your broker just forwarded a name: "Use this QI—they're fast and cheap."

You stare at the email. The industrial property you've held for eleven years is about to sell for $2.4 million more than you paid. That gain represents your entire down payment on the replacement asset in Katy. One procedural mistake—one moment where proceeds touch your account or your agent's control—and up to 40% of that gain vanishes to federal and state taxes.

Is "fast and cheap" really the standard you want for protecting $960,000 in equity?

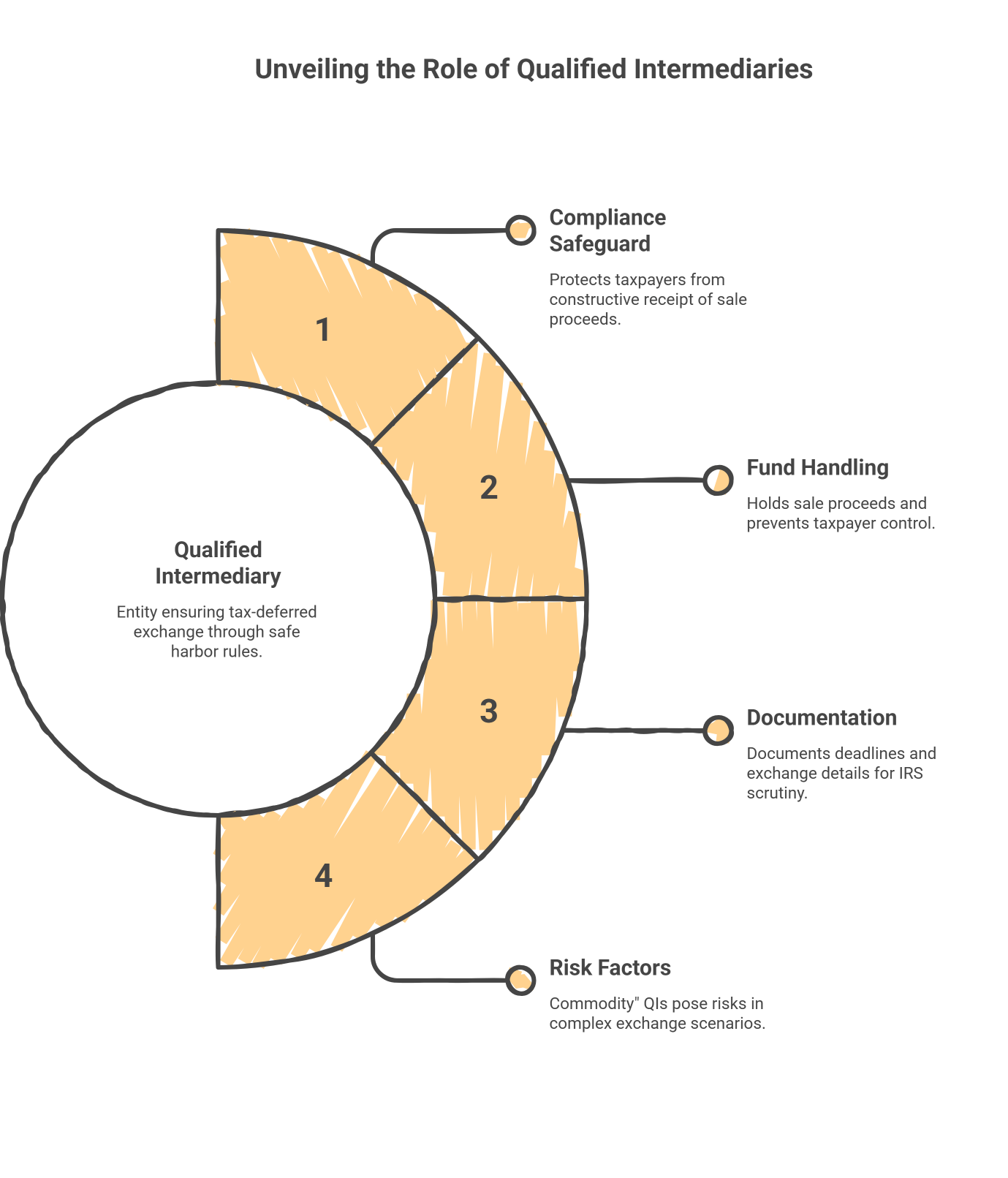

A Qualified Intermediary (QI) is an independent third party that facilitates a 1031 exchange by holding sale proceeds and coordinating exchange documentation so the taxpayer does not receive or control the funds—helping avoid constructive receipt and stay within the exchange rules.

The 1031 exchange industry has convinced property owners that Qualified Intermediaries are interchangeable vendors—a commodity service where the only variables are price and turnaround time. That myth is dangerous. And for developers running reverse exchanges, improvement deals, or any transaction with tight Houston closing timelines, it can be catastrophic.

Should QI selection matter for your transaction? Three checks:

The transaction has tight closing windows or multiple moving parts (broker, title, lender, CPA)

The plan involves buying first (reverse exchange) or using proceeds for improvements (construction/improvement exchange)

The exchange proceeds represent equity where process failure is not an option

If any of these apply, the "fast and cheap" QI your broker recommended may lack the legal structure, fund controls, or operational capability to protect your exchange. The next step is to vet before you close—not after.

What a Qualified Intermediary Actually Does—And When "Commodity" Selection Becomes Dangerous

A Qualified Intermediary is a 'safe harbor' entity defined under Treasury Regulation § 1.1031(k)-1(g)(4). While the use of a QI is not strictly 'required' by the tax code to perform an exchange, it is the most practical and universally used method to ensure the taxpayer does not have actual or constructive receipt of money or other property. By following the specific safe harbor rules—which include a written exchange agreement and restricted access to funds—the QI is treated as the person from whom the taxpayer receives the replacement property, ensuring the transaction is not treated as a taxable sale. [Treas. Reg. § 1.1031(k)-1(g)(4)(i)]. Without a properly structured QI arrangement, you have constructive receipt of the sale proceeds—and your exchange fails before it begins.

The QI functions as your compliance safeguard, sitting between you and the IRS's constructive receipt rules. The QI holds your sale proceeds, documents every deadline, and structures the exchange so you never have actual or constructive control of the funds. When this process works, you defer your entire gain. When it fails—because of weak fund controls, sloppy documentation, or a QI that lacks the legal capability to handle your deal structure—you write a check to the IRS instead of reinvesting in your next project.

When a "commodity QI" creates real risk:

Your deal involves a reverse exchange requiring an Exchange Accommodation Titleholder (EAT) and title parking

You need improvement exchange capability with controlled construction draws

Your closing timeline is compressed and requires precise coordination between title, lender, and QI

You want segregated fund accounts rather than commingled proceeds

You need audit-ready documentation that can withstand IRS scrutiny

The Commodity Myth: Why "Any QI Will Do" Is the Most Expensive Advice You'll Take

The pitch sounds reasonable. A title company affiliate offers QI services bundled with your closing. A national provider advertises flat-rate pricing. Your CPA mentions a firm that "handles these all the time."

The implicit message: Qualified Intermediaries are fungible. Pick the cheapest one and move on.

This framing misunderstands what a QI actually does—and what can go wrong when the wrong one handles your transaction.

The myth says: QI selection is a procurement decision based on price and convenience.

The reality: QI selection is a compliance decision based on fund controls, documentation discipline, and structural capability.

For a straightforward forward exchange—sell one property, buy another within 180 days—a basic QI may perform adequately. But Houston's commercial real estate market rarely produces straightforward deals. Value-add operators acquire properties that need renovation before they qualify as replacement assets. Developers find replacement properties before their relinquished properties sell. Family entities need to restructure ownership as part of the exchange.

These scenarios require a QI with capabilities that "commodity" providers typically lack: the ability to serve as an Exchange Accommodation Titleholder, administer construction draws with proper controls, and produce documentation that demonstrates compliance at every step.

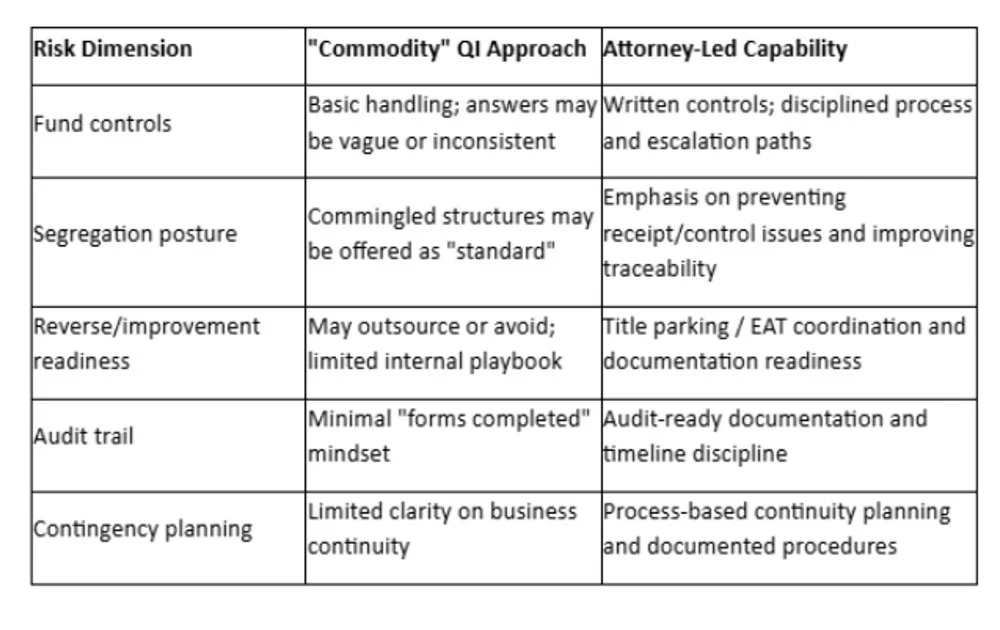

QI Risk Comparison: Commodity vs. Attorney-Led

Note: This matrix is a general risk framework, not a claim about any specific QI. Actual practices vary by firm and structure.

The attorneys and CPAs at Securitas 1031 regularly see exchanges that failed not because the investor made a mistake, but because their QI couldn't execute the structure the deal required.

What the IRS Actually Cares About: Constructive Receipt and the Safe Harbor That Protects You

The IRS doesn't care whether your QI was expensive or cheap, fast or slow. The IRS cares about one question: Did you have actual or constructive receipt or control of the sale proceeds at any point before acquiring your replacement property?

Constructive receipt means you had control over the funds—or could have had control—even if you never touched them. If your sale proceeds hit an account where you're a signatory, you have constructive receipt. If your attorney holds the funds without proper QI documentation, you have constructive receipt. If your QI's procedures allow you to demand the funds before the exchange period ends, you may have constructive receipt.

Once constructive receipt occurs, your exchange is disqualified. The entire gain becomes taxable in the year of sale.

The Treasury Regulations establish a safe harbor that protects taxpayers who use a properly structured Qualified Intermediary. To stay within this safe harbor, the QI must:

Be an independent party with no disqualifying relationships to the taxpayer

Hold exchange proceeds under a written exchange agreement

Acquire the relinquished property from the taxpayer and transfer it to the buyer

Acquire the replacement property and transfer it to the taxpayer

Maintain restrictions that prevent the taxpayer from receiving funds before the exchange completes

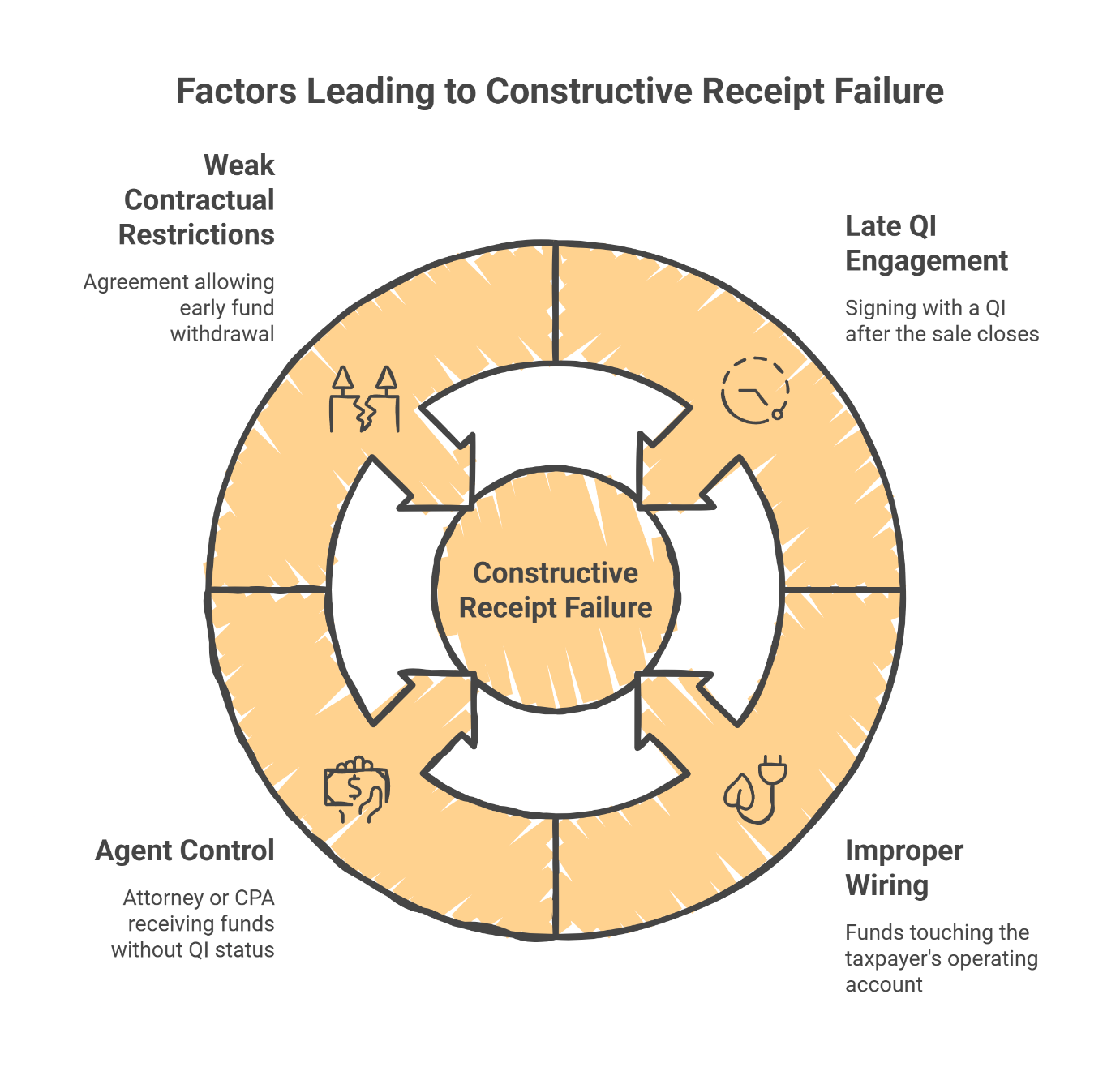

Common Paths to Constructive Receipt Failure

Late QI engagement. The exchange agreement must be in place before closing. If you sign with a QI after the sale closes, the safe harbor doesn't apply.

Improper wiring. Sale proceeds must go directly to the QI's qualified escrow or trust account. If funds touch your operating account—even briefly—the exchange fails.

Agent control. If your attorney, CPA, or other agent receives the funds without being the QI, you have constructive receipt through your agent.

Weak contractual restrictions. If your exchange agreement allows you to demand funds before identifying replacement property or before the 180-day deadline, you may have constructive control.

These aren't hypothetical risks. They're the actual failure modes that experienced 1031 exchange professionals encounter regularly. The discipline required to avoid them is why QI selection matters. For a detailed breakdown of the timeline requirements that create these pressure points, see our guide on building a strategic timeline for a flawless 1031 exchange.

The Hidden Risk in "Commodity" QIs: Fund Handling and Creditor Exposure

Beyond constructive receipt, there's a second category of risk that most property owners never consider: What happens to your exchange proceeds while the QI holds them?

In a typical exchange, the QI may hold your funds for weeks or months. During that time, two questions determine whether your equity is protected.

Are your funds segregated or commingled?

Some QIs maintain separate, client-specific accounts for each exchange. Others pool client funds into a single operating account and track ownership through internal ledgers.

Segregated accounts provide a clear chain of custody. Your funds sit in an account with your name on it, held by a qualified custodian bank. If the QI faces financial difficulty, your segregated funds are identifiable and separable from the QI's assets.

Commingled accounts create creditor exposure. If the QI faces bankruptcy, lawsuit judgments, or operational failure, your funds may be entangled with other clients' funds and the QI's own assets. Recovery becomes a legal process rather than a simple wire transfer.

What controls prevent unauthorized access?

Responsible QIs implement dual-signature requirements, written authorization procedures, and reconciliation protocols that prevent any single person from moving funds without oversight. They use qualified escrow or trust arrangements governed by written agreements that specify exactly when and how funds can be released.

"Commodity" QIs may lack these controls. In the worst cases, a single employee can wire funds without independent verification—creating fraud exposure and operational risk that has nothing to do with IRS compliance.

The Bankruptcy Scenario Property Owners Never Consider

What happens if your QI files for bankruptcy while holding your exchange proceeds? The answer depends entirely on how the QI structured its fund-holding arrangements. If funds were held in a properly documented qualified escrow or trust, they may be protected from creditor claims. If funds were commingled with operational assets, they may become part of the bankruptcy estate.

This isn't theoretical. QI bankruptcies have occurred, and property owners have lost exchange proceeds. The Wells Fargo Corporate Trust due diligence guidance on evaluating QIs emphasizes fund segregation and custodial arrangements as threshold requirements for responsible selection.

A Note on Bonding and Insurance

Many QIs cite fidelity bonds, errors-and-omissions coverage, or similar protections. Insurance is not a substitute for strong controls. Coverage can have exclusions, limits, and claims processes that may not align with transaction urgency. Request coverage details in writing and clarify what controls are required to keep coverage effective.

Why Attorney-Led Structuring Matters in Reverse and Improvement Exchanges

For a forward exchange—sell first, then buy—a competent QI with adequate fund controls may suffice. But many Houston developers and value-add operators face more complex scenarios that require capabilities beyond basic exchange facilitation.

Reverse Exchanges: Buying Before You Sell

In a reverse exchange, you acquire the replacement property before selling your relinquished property. This creates a structural problem: you can't own both properties simultaneously without triggering constructive receipt of the sale proceeds.

The safe harbor for reverse exchanges was established under IRS Revenue Procedure 2000-37. This procedure allows an Exchange Accommodation Titleholder (EAT) to 'park' title to a property for up to 180 days. It is important to note that while Rev. Proc. 2000-37 provides the safe harbor, the IRS also issued Rev. Proc. 2004-51, which clarifies that the safe harbor does not apply if the taxpayer already owned the replacement property within the prior six months. [IRS Rev. Proc. 2000-37; Rev. Proc. 2004-51]. The EAT takes title to either the replacement property (while you arrange the sale of your relinquished property) or the relinquished property (while you close on your replacement property). After the sale completes, the EAT transfers the parked property to complete the exchange.

This structure requires:

An entity qualified and willing to serve as the EAT

Title insurance that covers the parking arrangement

Loan structures that accommodate the EAT's temporary ownership

Documentation that demonstrates compliance with the Rev. Proc. 2000-37 safe harbor

Timeline management to ensure both legs close within 180 days

Many "commodity" QIs don't offer EAT services. Others offer them through affiliates or third parties without the documentation discipline to demonstrate safe-harbor compliance. If you need a reverse exchange and your QI can't provide EAT capability with proper legal structuring, you're working with the wrong QI.

Improvement Exchanges: Building Your Replacement Property

An improvement exchange allows you to use exchange proceeds not just to acquire a replacement property, but to improve it. You might buy land and construct a building, or acquire an existing property and complete a major renovation.

This structure requires the QI (or an EAT) to hold title to the replacement property while improvements are made using exchange funds. The QI must administer construction draws, ensure proper documentation of each disbursement, and transfer the improved property to you before the 180-day deadline.

The compliance requirements are substantial. Draw requests must be verified. Disbursements must be documented. The final property must qualify as "like-kind" real property under IRS rules. Without attorney-led oversight and documented procedures, improvement exchanges create significant audit exposure.

Why "Title Company Convenience" Isn't the Same as Legal Capability

Title company affiliates and national QI chains often emphasize their integration with the closing process. This convenience has value—but convenience isn't compliance.

Attorney-led QIs bring legal judgment to complex exchange structures. They can evaluate whether a proposed arrangement satisfies safe-harbor requirements, identify documentation gaps before they become audit problems, and provide escalation paths when deals encounter unexpected complications.

For straightforward forward exchanges, this legal capability may be unnecessary. For reverse exchanges, improvement exchanges, or any transaction with structural complexity, attorney-led oversight is often the difference between a successful exchange and an expensive tax bill. Our team of attorneys and real estate professionals at Securitas 1031—led by founder Charles H. Mansour with over 30 years of experience, 18,000+ closings, and $3 billion in transactions—has structured thousands of these complex transactions for Houston property owners.

Risk-Based Decision Matrix: 10 Questions That Separate Secure QIs from Commodity Vendors

Before you sign with any Qualified Intermediary, ask these ten questions. The answers will reveal whether you're working with a compliance-focused professional or a commodity vendor.

How to Score Answers

Green (strong controls): Clear, written, specific answers; control owners identified; process documented.

Yellow (adequate but limited): Partial clarity; answers rely on verbal assurances; documentation thin.

Red (inadequate or unclear): Vague answers; reluctance to provide details; "trust us" posture.

The 10 Questions

1. Where are my exchange proceeds held?

Look for: segregated, client-specific accounts at a qualified custodian bank. Red flag: commingled operating accounts or unclear fund-holding arrangements.

2. Is this a qualified escrow or trust arrangement, and what documents govern it?

Look for: written escrow or trust agreements that specify fund-handling procedures and release conditions. Red flag: informal arrangements or verbal assurances.

3. Who has signatory authority over my funds?

Look for: dual-signature requirements with independent verification. Red flag: single-person authorization or unclear control structures.

4. What written procedures exist for wiring, approvals, and reconciliation?

Look for: documented standard operating procedures with audit trails. Red flag: "we handle it on a case-by-case basis."

5. What bonding and insurance do you carry, and what does it not cover?

Look for: fidelity bonds and errors-and-omissions coverage with clear limits. Red flag: vague assurances or coverage that excludes common risk scenarios.

6. Do you provide audit-ready documentation?

Look for: comprehensive exchange files with timelines, notices, identification letters, and proof of delivery. Red flag: "we can pull something together if you need it."

7. Can you support reverse exchange structures consistent with Rev. Proc. 2000-37?

Look for: in-house EAT capability with documented safe-harbor procedures. Red flag: "we'd need to bring in a third party" or unfamiliarity with the safe-harbor requirements.

8. Can you support improvement exchange draw administration?

Look for: documented draw procedures with verification requirements and compliance controls. Red flag: "we don't really do those" or unclear disbursement procedures.

9. What is your contingency plan for incapacity, sale, or insolvency?

Look for: documented succession plans, backup QI arrangements, and fund-protection mechanisms. Red flag: "that's never happened" or no documented contingency.

10. Who provides oversight and escalation for complex exchanges?

Look for: attorney involvement in structuring decisions and escalation paths for unusual situations. Red flag: "our processors handle everything."

Scoring Guidance

8-10 Green answers: This QI demonstrates the fund controls, documentation discipline, and structural capability required for complex exchanges.

5-7 Green answers: This QI may be adequate for simple forward exchanges but likely lacks capability for reverse or improvement structures.

Fewer than 5 Green answers: Find a different QI. The risks to your exchange proceeds and compliance posture are too high.

For a deeper dive into the security questions that matter most, see our related article on how to choose a qualified intermediary.

What to Do Next: A Practical 30-Minute Vetting Workflow Before You Close

You don't need weeks to vet a Qualified Intermediary. You need 30 focused minutes and a willingness to ask direct questions.

Step 1: Build Your Shortlist (5 minutes)

Identify 2-3 QI candidates. Sources: your CPA's recommendations, your real estate attorney's referrals, or operators in your network who have completed similar exchanges. Avoid defaulting to whoever your title company suggests—that relationship serves the title company's convenience, not your compliance needs.

Step 2: Request Fund-Control Answers in Writing (10 minutes)

Email each candidate the first five questions from the vetting checklist above. Request written responses. A QI that can't articulate its fund-handling procedures in writing probably doesn't have documented procedures. Written answers do two things: prevent later misunderstanding, and establish whether documentation discipline exists from the start.

Step 3: Confirm Complex Capability If Needed (10 minutes)

If your exchange involves reverse or improvement structures, ask questions 7-10 directly. Get specific: "Can you serve as the EAT, or would you bring in a third party? What documentation do you provide to demonstrate Rev. Proc. 2000-37 compliance?"

A competent QI will answer these questions confidently and specifically. A commodity vendor will hedge, defer, or express unfamiliarity with the requirements.

Step 4: Engage Before Closing (5 minutes)

Once you've selected your QI, execute the exchange agreement before your sale closes. The safe-harbor protections require the QI relationship to be in place before proceeds change hands. Waiting until closing day to "figure out the QI situation" is how exchanges fail. Our guide on managing the closing gap covers the coordination required to keep your exchange on track.

Houston-Specific Coordination Reality

In Houston's commercial market, tight closing timelines are normal. Your broker, title company, lender, and CPA all have their own deadlines and requirements. Adding a QI to this coordination challenge requires advance planning.

Alert your QI to expected closing dates as early as possible. Confirm wiring instructions before closing day. Ensure your title company knows to wire proceeds directly to the QI's qualified escrow account—not to your operating account "to be forwarded."

The operators who execute 1031 exchanges successfully treat QI selection as a Day One decision, not a Day Before Closing scramble. Resources like our continuing education courses help brokers and advisors understand these coordination requirements.

From Commodity Thinking to Compliance Confidence

The "commodity QI" myth persists because it's convenient. It lets property owners treat a compliance decision like a procurement decision—find the cheapest vendor, check the box, and move on.

But you're not checking a box. You're protecting equity that took years to build. You're preserving capital that funds your next acquisition, your next development, your continued portfolio growth.

The QI you select determines whether that equity stays in your control or becomes a tax payment. Fund controls matter. Documentation discipline matters. Attorney-led structuring matters—especially when your deal involves reverse exchanges, improvement structures, or the tight closing timelines that define Houston's commercial real estate market.

Vet before you close. Ask the hard questions. And choose a Qualified Intermediary whose capabilities match the complexity of your exchange.

That's how you keep your equity working for you.

Ready to discuss your exchange structure with an attorney-led QI team?

Schedule a Free In-Person Consultation with Securitas 1031. We'll review your transaction, identify potential compliance risks, and explain exactly how we'd structure your exchange to protect your proceeds.

Securitas 1031 440 Louisiana St, Suite 1100 Houston, TX 77002 Tel: 713-275-8112

Disclaimer: This article provides general information about 1031 exchanges and does not constitute tax or legal advice. For a detailed analysis of your specific situation, consult a licensed tax professional or 1031 exchange accommodator.

Our Editorial Process

Our expert team uses AI tools as a supplement to ensure accuracy and clarity, but every article is reviewed by a real person with 1031 exchange expertise before publication.

By: Securitas 1031 Team

Securitas 1031 supports direct property owners with attorney-led 1031 exchange structuring, documentation discipline, and consultation-first execution designed to reduce compliance and fund-handling risk.