Reverse 1031 Timeline: How to Close on the New Asset First

📌 Key Takeaways

A reverse 1031 exchange lets you buy your new property first, but every step must happen in exact order before you close.

Structure Before You Close: The Exchange Accommodation Titleholder, all paperwork, and funding must be ready before Day 0—you can't fix anything after closing.

Day 45 Means What You'll Sell: Unlike a regular exchange where you identify what to buy, here you identify what property you plan to sell within 45 days of closing.

Day 180 Is the Hard Stop: If your old property doesn't sell by Day 180, the exchange fails and you owe taxes on your entire gain.

Cash Hits You Early: You pay for the new property upfront and won't get money back until your old property sells—plan for this gap.

Your QI Starts the Clock: Engage your Qualified Intermediary weeks before closing to form entities, draft documents, and coordinate with lenders and title companies.

Miss one deadline or skip one step, and the entire tax deferral disappears.

Property owners pursuing competitive acquisitions will find the complete timeline and coordination checklist below, preparing them for a compliant reverse exchange from first wire to final transfer.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

The wire instructions are due tomorrow. The Exchange Accommodation Titleholder isn't formed yet. The lender is asking questions about vesting that nobody on your team can answer.

This is what happens when a reverse 1031 exchange gets treated like a standard deal with paperwork added at the end. The sequence matters. The deadlines are fixed. And the consequences of getting it wrong—immediate tax liability on the entire gain—don't negotiate.

A reverse 1031 exchange lets you close on your replacement property before selling your current one. For property owners pursuing competitive acquisitions in the Houston market, that flexibility can mean the difference between securing the right asset and losing it to a faster buyer. But the IRS requires a specific structure, and the timeline is unforgiving.

Here's the roadmap: what must happen before Day 0, what triggers your deadlines, and how to keep the entire transaction compliant from first wire to final transfer.

What Makes a Reverse 1031 Exchange Different

You acquire the replacement property before disposing of the relinquished one—the opposite of a standard deferred exchange where you sell first and buy later.

The IRS doesn't allow you to hold title to both properties simultaneously (outside narrow exceptions). So a reverse exchange requires a "parking" arrangement: an Exchange Accommodation Titleholder (EAT) temporarily holds title to one of the properties while you complete the transaction.

Most reverse exchanges follow the safe-harbor framework established in IRS Revenue Procedure 2000-37, which outlines the Qualified Exchange Accommodation Arrangement (QEAA) structure, along with modifications in IRS Revenue Procedure 2004-51. This isn't optional flexibility—it's the compliance foundation that keeps your tax deferral intact.

The critical difference from a forward exchange: you cannot close on the new asset and "fix the paperwork later." The EAT, the documentation, and the funding structure must exist before the replacement property closes.

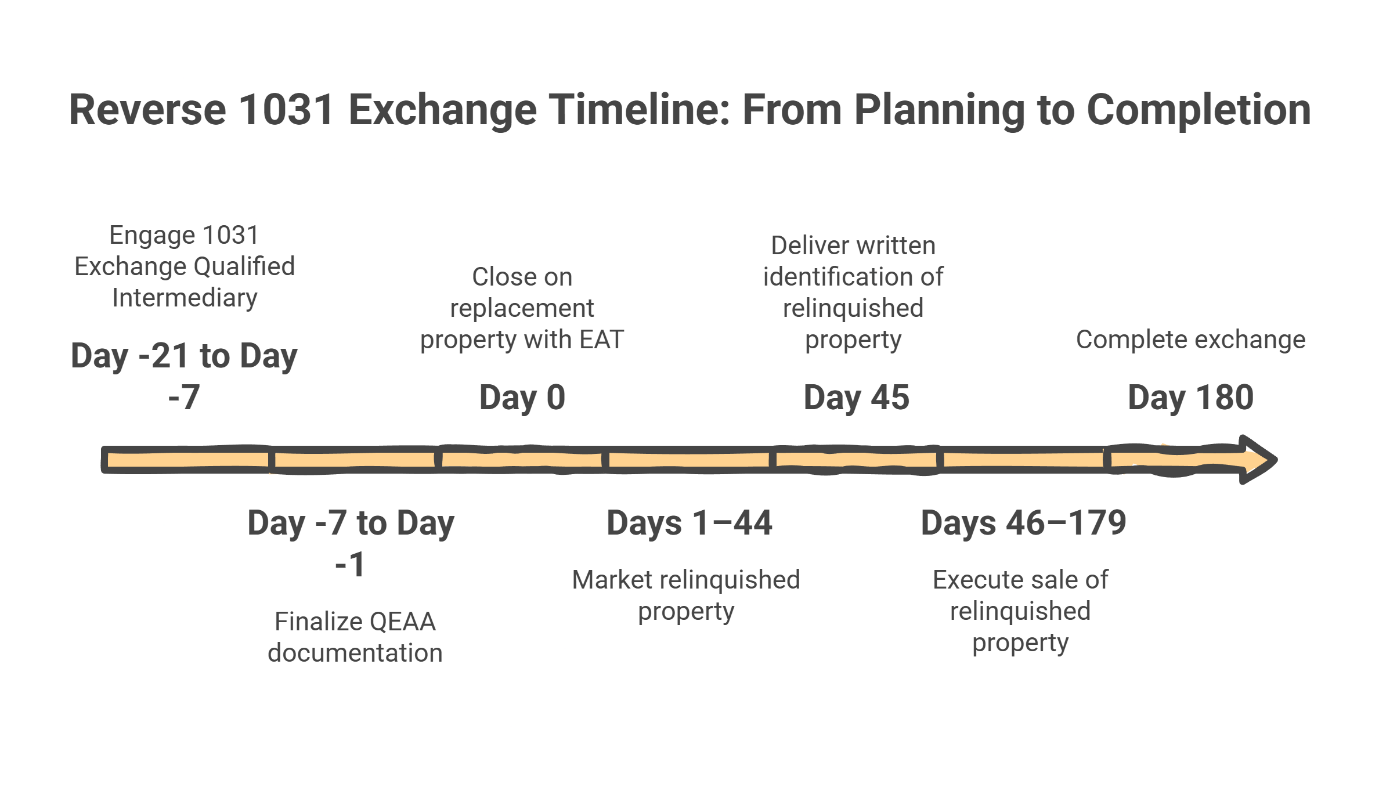

Reverse 1031 Timeline at a Glance

Here's the sequence from planning through completion:

Day -21 to Day -7: Engage your 1031 Exchange Qualified Intermediary and begin EAT formation, document drafting, and lender/title coordination.

Day -7 to Day -1: Finalize the QEAA documentation package, confirm funding sources, and align closing statement language with title.

Day 0: Close on the replacement property with the EAT taking title under the parking arrangement.

Days 1–44: Market your relinquished property and finalize your disposition plan.

Day 45: Deliver written identification of the potential relinquished property (or properties) to be sold (hard deadline)

Days 46–179: Execute the sale of your relinquished property and coordinate the transfer.

Day 180: Complete the exchange—relinquished property sold, parked property transferred to you (hard deadline).

Miss Day 45 or Day 180, and the exchange fails. There are no extensions.

Think of the timeline as two parallel tracks running simultaneously. Track A covers the replacement property: setup and coordination through Day 0, then the parked period while the EAT holds title. Track B covers the relinquished property: disposition planning and marketing preparation before Day 0, the identification deadline at Day 45, and the sale closing before Day 180. Both tracks must reach completion for the exchange to succeed.

Step 1: Engage a Qualified Intermediary Before You Lock a Closing Date

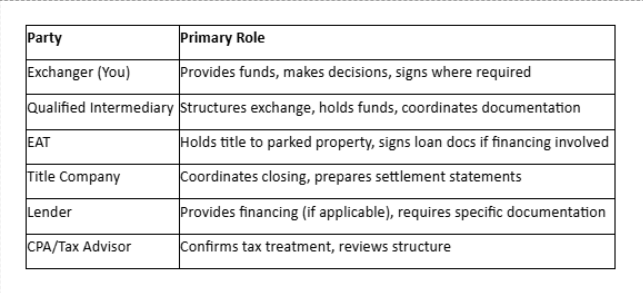

The qualified intermediary coordinates the documentation workflow, holds exchange funds to prevent constructive receipt, and ensures the legal structure satisfies IRS requirements.

In a reverse exchange, the QI's role expands. They typically work alongside (or provide) the EAT entity, draft the exchange agreement and QEAA documents, coordinate with title and lender on vesting and closing language, and establish the funding and wiring sequence.

Our attorney-led team in Houston structures these transactions with a focus on documentation discipline—because reverse exchanges expose gaps that standard deals often hide.

Who does what in a reverse exchange:

Step 2: Pre-Closing Requirements Checklist

Before Day 0, these elements must be in place:

EAT entity formed and ready to take title

QEAA documentation package drafted (exchange agreement, parking arrangement, assignments)

Funding plan confirmed—who wires what, when, and to which account

Lender approvals secured (if financing the replacement property)

Title coordination complete—vesting instructions, closing statement language aligned

Wiring instructions verified—especially critical for Houston closings with same-day funding requirements

The order of operations is unforgiving. Funding must precede closing.

If your lender hasn't approved the EAT structure or your title company hasn't received proper vesting instructions, you're not ready to close—regardless of what the purchase contract says.

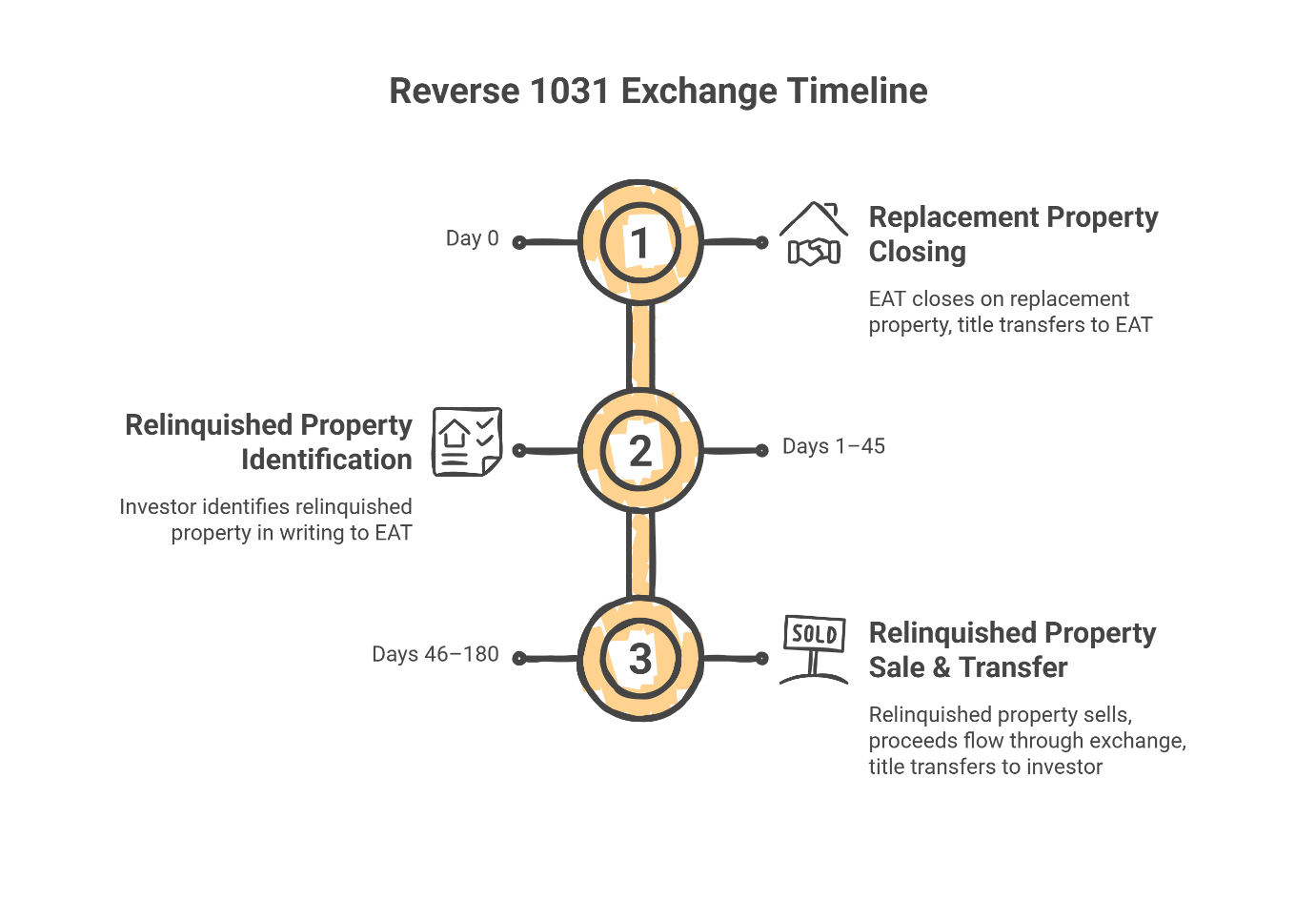

Day 0: Closing on the Replacement Property

On Day 0, the EAT closes on your replacement property. Title transfers to the EAT under the parking arrangement, not directly to you.

What this means for your cash flow:

Your capital outlay at Day 0 typically includes the down payment (if financing) or full purchase price (if cash), closing costs and title fees, lender-required reserves, and QI/EAT fees.

These costs hit immediately. You won't recover them until the relinquished property sells and the exchange completes. Whether you're an individual investor upgrading from a single rental property or a family selling a commercial building you've held for decades, budget for this liquidity requirement separately from your standard acquisition planning.

Days 1–45: Identify the Relinquished Property

Here's where reverse exchanges trip up even experienced property owners: you're not identifying what you want to buy. You're identifying what you plan to sell.

Within 45 days of the replacement property closing, you must deliver written identification of the relinquished property (or properties) you intend to dispose of to complete the exchange. The same identification rules from Treasury Regulation §1.1031(k)-1 apply—including the three-property rule (identifying up to three properties of any value) and the 200% rule (identifying any number of properties whose aggregate fair market value does not exceed 200% of the relinquished property's value). For additional background on like-kind requirements, see the IRS Like-Kind Exchanges overview.

This deadline is absolute. Unlike standard tax filing deadlines, 1031 exchange deadlines are calculated in strict calendar days. If Day 45 falls on a Saturday, Sunday, or legal holiday, the deadline does not extend to the next business day. You must submit your identification by midnight on that specific calendar date. Treating the deadline as flexible is not just a strategic risk—it is a compliance failure.

It's 4:45 PM on Day 44. Your identification letter isn't signed. The fax machine is jammed. This scenario plays out more often than it should. Build your deadline management into the calendar from Day 1, not Day 40.

For detailed deadline strategies, see Beat the clock: a strategic 1031 timeline.

Days 46–180: Sell the Relinquished Property and Complete the Transfer

After Day 45, your focus shifts entirely to disposition. The relinquished property must sell, close, and the proceeds must flow through the exchange structure before Day 180.

If the sale doesn't close inside the window, the exchange fails. The parked property cannot transfer to you tax-deferred. If you have sold the relinquished property, the gain becomes immediately taxable. If you have not sold it, you simply retain ownership of both assets—a liquidity crisis rather than a tax event.

The domino effect of a failed sale:

The EAT still holds title to your replacement property. You've already funded the acquisition. But without a completed exchange, the tax deferral collapses. You may still acquire the property, but you'll owe capital gains tax on the relinquished property sale—exactly what the exchange was designed to avoid.

This is why your disposition plan must be real before you commit to Day 0. "We'll figure out how to sell it later" is not a compliant strategy.

Cash-Flow Planning for Your Exchange

Before committing to a reverse exchange, confirm these liquidity requirements:

Immediate capital for replacement property acquisition (Day 0)

Carrying costs for the parked property during the exchange period

Marketing and transaction costs for the relinquished property sale

Contingency reserves if the relinquished property sale takes longer than expected

QI and EAT fees (typically due at closing)

Also build a backup disposition plan. What happens if your primary buyer falls through on Day 120? Having a secondary exit strategy—even at a reduced price—protects the entire exchange and preserves your family's wealth.

Reverse transactions pull cash forward. Even with financing, liquidity planning should assume uncertainty on both sides: timing of the relinquished sale and timing of any reimbursements under the planned documentation approach. The safe move is to plan for higher up-front liquidity than a forward exchange would require.

Common Reverse Timeline Failure Points

Most failures are execution problems—calendar control, documentation control, and closing coordination—not tax theory problems.

These mistakes collapse reverse exchanges:

Waiting to engage the QI until the purchase contract is signed. By then, you may not have enough lead time to form the EAT and complete documentation.

No real disposition plan. Hoping the relinquished property sells isn't a strategy.

Title and lender misalignment. If the lender won't accept the EAT structure or title won't prepare proper vesting, you can't close compliant.

Documentation gaps. Missing assignments, unsigned agreements, or incomplete QEAA packages create constructive receipt risk—and weaken your audit-defensible position if the IRS reviews the transaction.

For coordination strategies across your broker, title company, lender, and QI, see Managing the closing gap.

Houston Execution Notes

Houston-area transactions move fast. A few execution points specific to this market:

Wiring timing: Many Houston title companies have afternoon wire cutoffs. If you're targeting a same-day close, confirm cutoff times with title at least 48 hours in advance.

Same-day funding: Lenders may require same-day funding confirmation before releasing loan proceeds. Coordinate this with your QI to ensure exchange funds are positioned correctly.

Title coordination: Houston title companies vary in their familiarity with EAT structures. Work with a title company that has closed reverse exchanges before—or ensure your QI can provide the necessary coordination and documentation.

Frequently Asked Questions

When does the reverse exchange timeline officially start?

Day 0 is the closing date for the replacement property—the date when the EAT takes title under the parking arrangement. All deadlines (Day 45, Day 180) count forward from that date.

What must be done before Day 0?

The EAT must be formed, QEAA documentation must be drafted and signed, funding must be arranged, and title/lender coordination must be complete. You cannot close compliant without this foundation.

What exactly must be identified by Day 45?

The relinquished property (or properties) you intend to sell to complete the exchange. You're identifying what to sell, not what to buy.

What happens if the relinquished property doesn't sell by Day 180?

The exchange fails. You cannot transfer the parked property tax-deferred, and you'll recognize gain on the relinquished property sale.

Can I hold title to both properties at the same time?

Generally, no—not if you want to stay within the IRS safe harbor. The EAT structure exists specifically to avoid simultaneous ownership.

How does financing work when the EAT holds title?

The EAT typically signs the loan documents as the titleholder. Lender approval of this structure is required before closing—another reason to start QI engagement early.

Your Next Step: Map the Dates

A reverse 1031 exchange gives you acquisition speed. But that speed requires structure, documentation, and deadline discipline from day one.

The sequence is fixed: EAT and funding before Day 0. Identification by Day 45. Sale and transfer complete by Day 180. Get any of these wrong, and the tax deferral disappears.

If you're planning a reverse exchange—whether you're an individual investor moving up to a larger property or a family repositioning assets for the next generation—start the conversation before you lock your closing date. Schedule a consultation with Securitas 1031 to map your dates, confirm your liquidity requirements, and build the documentation structure that keeps your exchange compliant. For a lower-commitment starting point, explore our continuing education course on 1031 timing and rules.

Further Reading:

Managing the Closing Gap: Coordinating Sale and Purchase Timelines

Beat the Clock: A Strategic Timeline for a Flawless 1031 Exchange

Disclaimer: This article is for educational purposes only and does not provide legal or tax advice. 1031 exchange rules are fact-specific and can change based on your transaction details. Before acting on any timeline or structure described here, consult your tax advisor and a qualified intermediary experienced in reverse 1031 exchanges.

Our Editorial Process:

Securitas 1031 content is developed using primary IRS guidance, Treasury regulations, and internal exchange procedures to explain technical topics in clear, practical language. We review drafts for terminology consistency and deadline accuracy, and we update published content when rules, guidance, or common transaction practices change. For transaction-specific guidance, schedule a consultation with our team.

By: The Securitas 1031 Insights Team.

Securitas 1031 is a Houston-based, attorney-led qualified intermediary that structures standard, reverse, and improvement 1031 exchanges for direct property owners, with a focus on secure handling of exchange funds and disciplined compliance workflows.