Securing Land Before You Sell: The Reverse Exchange Guide for Developers

📌 Key Takeaways

A reverse 1031 exchange lets you buy land before selling your current property—but only if you set up the right structure before closing.

Buy Through a Placeholder, Not Yourself: An Exchange Accommodation Titleholder (EAT) must take title to the new property first; if you close in your own name, you lose the tax deferral permanently.

Engage Your QI Before Signing: Your Qualified Intermediary needs to create the parking structure before you close on the land—retrofitting after purchase doesn't work.

Two Hard Deadlines Control Everything: You have 45 days to identify the property you'll sell and 180 days to complete the entire exchange; missing either deadline kills the deal.

Never Touch the Sale Proceeds: Money from your old property must flow through the QI—if it hits your account even briefly, the exchange fails and taxes come due immediately.

Run the Math First: Compare reverse exchange costs (typically $25K+) against potential tax savings (often $150K+); if fees exceed 40% of your deferral, reconsider.

Lock in the land you want without losing your tax deferral—just structure it right from day one.

Developers and investors facing timing gaps between finding the perfect replacement property and selling their current holdings will gain a clear compliance roadmap here, preparing them for the detailed planning steps that follow.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

The lot is perfect. The zoning works. The seller is motivated. There's just one problem—your capital is locked in a property that hasn't sold yet.

Waiting isn't an option. Another developer is circling. The entitlements timeline starts the moment you close. Every week of delay costs you momentum you can't recover.

A Reverse 1031 Exchange lets you acquire a replacement property before selling the relinquished property by using an Exchange Accommodation Titleholder (EAT) to "park" title temporarily. Under the IRS safe harbor framework established in Revenue Procedure 2000-37, this structure treats the EAT as the beneficial owner for tax purposes, allowing you to complete a qualifying exchange even when your timing runs backward.

But structure matters. Buy the land the wrong way—take title yourself, touch the proceeds, miss a deadline—and you've converted a timing problem into a six-figure tax bill. This guide walks you through how to do it right.

Diagnosing Your Current State

Before committing to a reverse exchange, you need to answer three questions honestly.

Is This a Timing Problem—or an Eligibility Problem?

A reverse exchange solves when you close. It doesn't solve whether you qualify.

The property you're selling must be held for investment or productive use in a trade or business. If you're flipping lots as inventory—buying and selling land as your primary business activity—you may be classified as a dealer, and dealer property doesn't qualify for 1031 treatment regardless of structure.

This distinction matters especially for developers. A developer who holds land for an extended period (e.g., over a year) primarily for appreciation is typically viewed as an investor, though significant development activity (like entitlements) can sometimes weigh toward dealer status. A developer who buys, subdivides, and sells parcels with high frequency is almost certainly a dealer. The IRS applies a multi-factor test to determine dealer status: holding period, frequency of sales, marketing efforts, and your primary income source. When dealer or inventory risk is present, the question becomes fact-specific and may vary by project and holding pattern.

If there's any ambiguity, involve your tax counsel before you structure the exchange. Retrofitting a reverse exchange after you've already taken title doesn't work.

What's Your Capital Gap?

A reverse exchange requires someone to fund the acquisition before your sale closes. That means understanding exactly where your capital sits:

How much equity is trapped in the relinquished property?

What's the purchase price of the replacement land?

Do you have bridge financing available, or will you need lender coordination with the EAT?

The EAT will hold title, but someone has to provide the acquisition funds. Options include loans from you to the EAT, third-party financing secured by a guarantee you provide, or partner capital. Each path has documentation requirements. The key planning question is practical: what funding path supports the acquisition closing without creating exchange-risky fund handling? Map yours before you're under contract pressure.

Have You Talked to Your Lender and Title Company?

Reverse exchanges add complexity to the closing flow. If utilizing third-party financing, the lender must lend directly to the EAT or consent to a back-to-back loan structure. Your title company needs to coordinate the parking arrangement documentation alongside standard closing documents.

Title companies, lenders, and counsel must align on who takes title at closing, the documented funding path, and the closing flow mechanics. This coordination is not optional—it's a requirement-driven workflow.

Surprises at the closing table kill deals. Brief your lender and title officer early—ideally before you sign the purchase contract.

What a Reverse 1031 Exchange Actually Does

A reverse exchange exists because of a simple rule: you cannot hold title to both the replacement property and the relinquished property at the same time and still qualify for 1031 treatment.

The workaround is title parking. An Exchange Accommodation Titleholder—typically a special-purpose LLC controlled by your Qualified Intermediary—acquires and holds the replacement property until your relinquished property sells. Once the sale closes, the exchange completes: proceeds flow through the QI, and the parked property transfers to you.

The EAT's Role

The EAT isn't a passive placeholder. Under Rev. Proc. 2000-37, the EAT must be treated as the beneficial owner of the parked property for all federal income tax purposes. This means the EAT reports the property's tax attributes, holds title in a manner consistent with ownership, and maintains the structure required for safe harbor protection.

You can still occupy or manage the property while it's parked—the revenue procedure explicitly permits lease-back arrangements and management agreements. But the ownership structure must be genuine, not a paper fiction.

Where the Qualified Intermediary Fits

The QI serves as the exchange facilitator, holding proceeds and coordinating the documentation that keeps you from constructive receipt. In a reverse exchange, the QI typically also controls the EAT entity.

This is where attorney-led oversight matters. Reverse exchanges involve layered agreements—the Qualified Exchange Accommodation Agreement, the EAT operating documents, loan arrangements, lease-back terms. A title company affiliate checking boxes isn't the same as a legal team that understands what happens when something goes sideways. The Securitas 1031 team brings 30+ years of experience and 18,000+ closings to these structures—the kind of depth that protects your exchange when complexity increases.

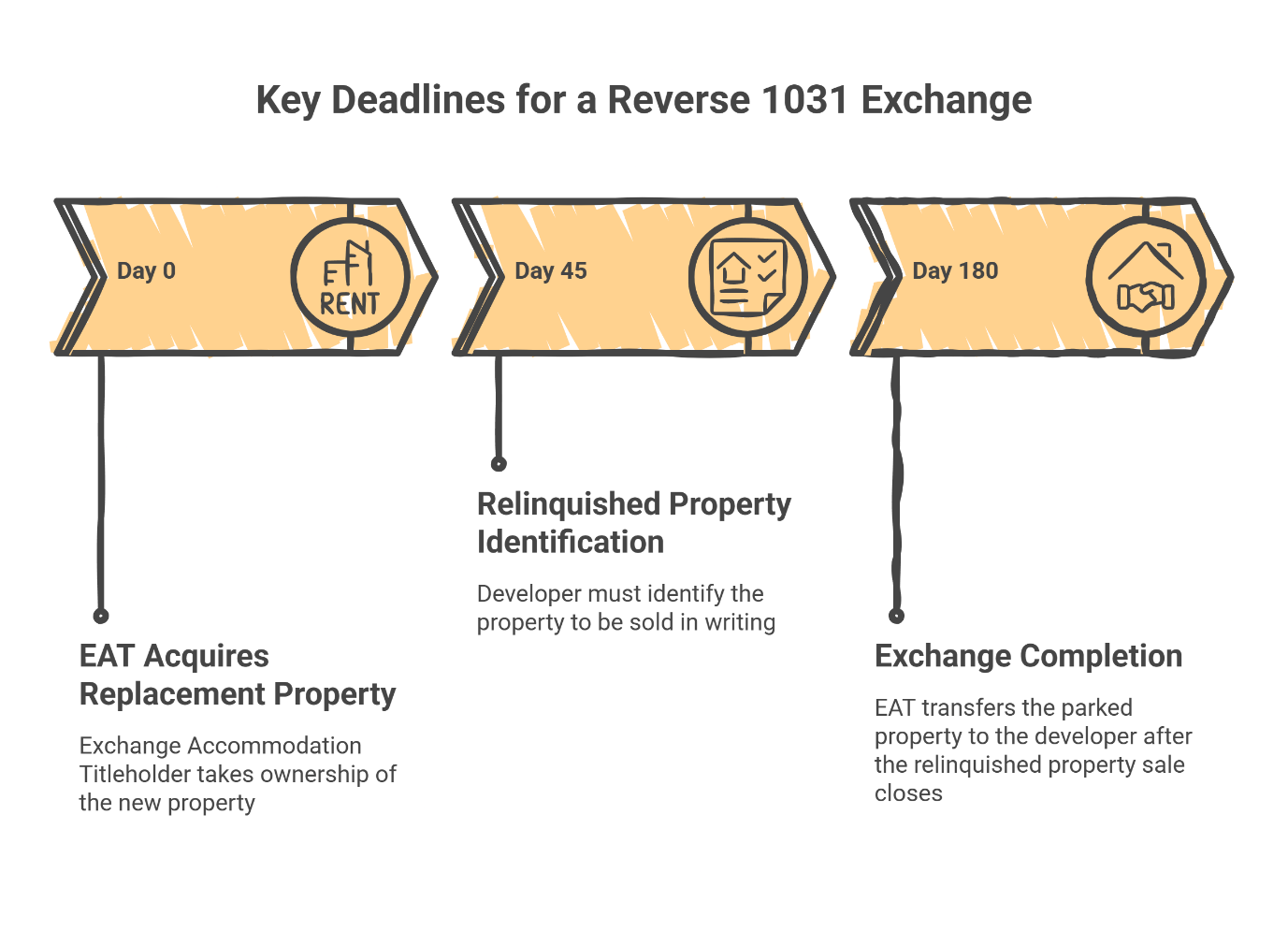

The Hard Deadlines

Two clocks start running when the EAT acquires the replacement property. These deadlines derive from the timing framework established in Treasury Regulation §1.1031(k)-1.

45-Day Identification Period: You must identify the relinquished property in writing within 45 days of the transfer of the replacement property to the EAT. The identification must be written, properly delivered, and consistent with the transaction structure. Miss this deadline by even one day, and your safe harbor protection disappears.

180-Day Exchange Period: The EAT must transfer the parked property to you—which means your relinquished property sale must close and the exchange must complete—within 180 days of the EAT's acquisition.

These aren't soft targets. Exceptions are extremely rare, limited primarily to Presidentially declared disasters or military service in combat zones. Aside from these specific statutory relief provisions, there are no extensions or 'substantial compliance' arguments that reliably work. Plan backward from day 180, not forward from day 1. For a deeper dive on deadline management, see our guide on strategic timeline planning.

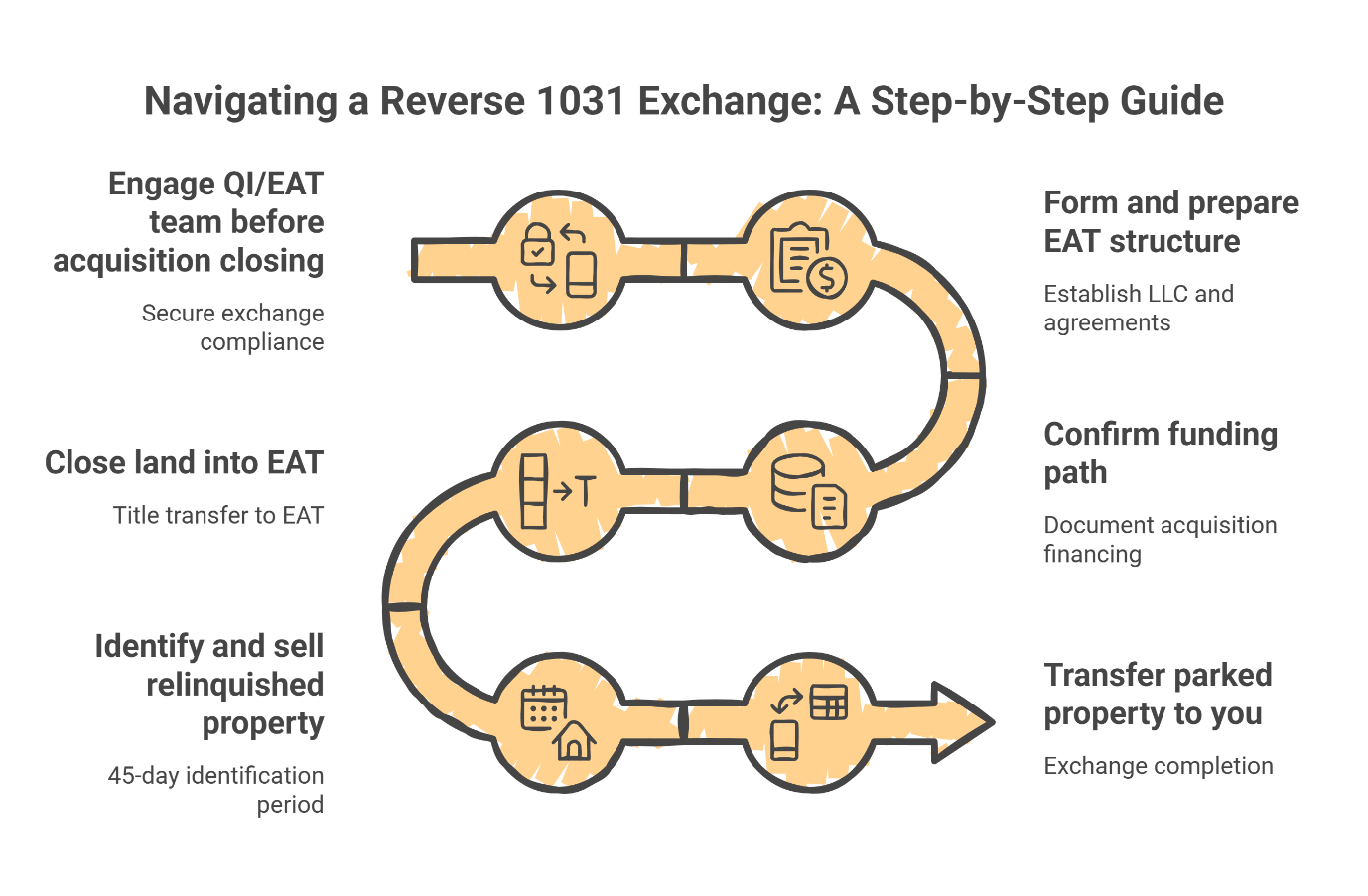

Steps to Initiate a Parking Arrangement

A reverse exchange is won or lost before the acquisition closing. Here's the sequence that keeps your exchange compliant:

Engage your QI/EAT team before the acquisition closing. The exchange accommodation agreement must be in place before title transfers to the EAT. Trying to paper a reverse exchange after you've already closed is too late. Engagement timing is a structural requirement, not a preference.

Form and prepare the EAT structure. Your QI will establish the single-member LLC that will hold title, draft the QEAA, and prepare the ancillary agreements (lease-back, management, indemnification).

Confirm the funding path. Document how the EAT will acquire the property—your loan, third-party financing, or a combination. Ensure your lender's documents contemplate the EAT structure. The specific structure depends on lender underwriting and closing logistics.

Close the land into the EAT. Title transfers to the EAT, not to you. The QEAA must be executed within five business days of this closing.

Identify and sell the relinquished property on schedule. You have 45 days to formally identify the relinquished property. Then execute the sale and ensure proceeds flow through the QI—not to you, not to your operating account, not anywhere that creates constructive receipt risk.

Transfer the parked property to you after disposition. Once the relinquished property closes and proceeds are properly handled, the EAT deeds the replacement property to you. The exchange is complete.

For additional reading on exchange strategies and timing coordination, visit the Build Wealth with 1031s resource library.

What Separates Successful Reverse Exchanges from Failed Ones

The difference between a compliant reverse exchange and a failed one usually comes down to preparation—specifically, when you engage your team and how thoroughly you've documented the structure before closing.

Last-minute engagement creates risk. When property owners sign purchase contracts before consulting a Qualified Intermediary, they often discover that their closing timeline, funding structure, or lender requirements don't align with reverse exchange documentation requirements. Scrambling to assemble the EAT structure in the final weeks before closing leaves no margin for error. This is where exchanges fail.

Early engagement creates options. Property owners who engage their QI before signing the purchase contract can build the structure properly from the start. Funding is documented. Lenders understand the EAT arrangement. The timeline accounts for both the 45-day identification requirement and the 180-day exchange period. Execution becomes methodical rather than reactive.

Ongoing relationships create efficiency. Property owners who execute multiple exchanges over time benefit from standing relationships with attorney-led QI teams. Lenders already understand the EAT structure. When the right property appears, the infrastructure is already in place. This preparation allows you to move decisively while others are still trying to determine whether a reverse exchange is even possible.

The pattern is consistent: reverse exchanges succeed when the QI is part of the planning process, not an afterthought.

Cost vs. Opportunity: When a Reverse Exchange Is Worth It

Reverse exchanges cost more than standard deferred exchanges. Typical components include:

QI and EAT administrative fees

Legal documentation (QEAA, entity formation, loan documents)

Lender fees for EAT-structured financing

Carrying costs during the parking period (interest, insurance, property taxes)

These costs are real. But so is the alternative.

The opportunity-cost lens: What does losing this site actually cost you? If the land fits your development criteria—zoning, location, basis for your pro forma—walking away means starting the search over. That's months of delay, plus the risk that comparable sites aren't available or are priced higher when you have liquidity.

The tax-deferral lens: A reverse exchange preserves your ability to defer gains on the relinquished property. On a $500,000 gain at a 30% combined rate, that's $150,000 of working capital you keep deployed instead of sending to the IRS.

The decision rule isn't "minimize cost." It's "maximize net outcome." If the reverse exchange fees are $25,000 and the tax deferral is $150,000, the ROI is obvious. If the fees approach the deferral amount or the deal economics are marginal, the math may not work.

Reverse Exchange Feasibility Calculator

Use these inputs to estimate your breakeven:

Input

Your Number

Estimated net gain on relinquished property

$_______

Estimated combined tax rate (federal + state)

_____%

Target land purchase price

$_______

Expected time-to-sale for relinquished property (days)

_______

Estimated reverse exchange fees (QI/EAT + legal)

$_______

Estimated carrying costs during EAT hold

$_______

Outputs to calculate:

Estimated tax deferred = Gain × Tax Rate

All-in reverse costs = Fees + Carrying Costs

Breakeven = Reverse Costs ÷ Tax Deferred

Decision guidance: If your all-in costs are under 20% of your tax deferral and you have a realistic path to selling the relinquished property within 120 days, proceed. If costs exceed 40% of deferral or your sale timeline is uncertain, validate eligibility and deal economics with your advisor before committing.

This tool provides a general estimate and does not constitute tax or legal advice. For a detailed analysis, consult a licensed tax professional or 1031 exchange accommodator.

The Scaling Roadmap: 90-Day Action Plan

Days 1–7: Feasibility and Eligibility Validation

Confirm the relinquished property qualifies (held for investment/business use, not dealer inventory)

Estimate gain, tax exposure, and reverse exchange cost range

Identify funding path for EAT acquisition

Days 8–21: Team Assembly and Timeline Mapping

Engage QI/EAT provider (attorney-led structure recommended)

Brief lender and title company on reverse exchange mechanics

Build backward timeline from day 180 target

Days 22–45: Acquisition Execution and Documentation

Execute purchase contract with closing into EAT

Finalize QEAA and ancillary agreements

Close replacement property into EAT

Formally identify relinquished property within 45-day window

Days 46–180: Disposition Execution and Transfer

Market and sell relinquished property

Ensure sale proceeds flow through QI (no constructive receipt)

Complete exchange and transfer parked property to you

Common Failure Points (and How to Prevent Them)

Missing deadlines. The 45-day and 180-day periods are statutory. Deadlines are strict calendar days; they do not extend for holidays or weekends (unless the deadline falls on one, per IRS rules, but relying on this is risky). Build buffer into your timeline—if you need 150 days to sell, you're already at risk.

Constructive receipt of funds. If you touch the sale proceeds—even briefly, even with good intentions—the exchange fails. Proceeds must flow through the QI. Your operating account should never see exchange funds.

Documentation gaps. The QEAA must be executed within five business days of the EAT's acquisition. Entity formation, loan documents, and lease-back agreements need to be in place at closing, not created after the fact. Sloppy paperwork creates audit exposure.

Related-party complications. If you're selling to or buying from a related party, additional rules apply. Rev. Proc. 2004-51 added restrictions specifically targeting certain related-party arrangements. These transactions aren't prohibited, but they require careful structuring.

Trying to fix it after you took title. If you already own the replacement property in your name, you can't retrofit a reverse exchange. The EAT must acquire the property—you can't park something you already hold. This is why QI engagement must happen before closing, not after.

For more on exchange pitfalls, see our guide on managing the closing gap.

Next Step: Get a Reverse Exchange Feasibility Review

If you're facing a timing gap between acquisition and disposition, the next step is a feasibility conversation—not a commitment. For developers and property owners in Houston, Austin, and San Diego, the most practical move is a review before signing or closing.

What to bring:

Purchase contract for the replacement property (or term sheet if not yet executed)

Estimated sale timeline and marketing status for the relinquished property

Estimated gain and basis information

Lender term sheet or financing parameters

What you'll get:

Timeline map showing your 45-day and 180-day windows

Feasibility calculator output for your specific numbers

Risk checklist highlighting structure and documentation requirements

Clear guidance on whether a reverse exchange fits your situation

Schedule your free consultation with Securitas 1031 before you sign or close. Our attorney-led team—with $3 billion in transactions and a partnership with Fidelity National Title since 2009—can help you evaluate whether a reverse exchange protects your deal or whether another path makes more sense.

Securitas 1031 also offers a free continuing education course, "An Overview of 1031 Exchanges," providing 1 Hour TREC CE Credit for real estate professionals seeking to deepen their understanding of exchange mechanics.

Securitas 1031, LLC 950 Echo Lane, Suite 200 Houston, TX 77024 832-544-6318

Disclaimer: This content is for informational purposes only and does not constitute legal, tax, or financial advice. 1031 exchange rules are highly technical and outcomes depend on your specific facts (including property descriptions, identification method, delivery/receipt process, and transaction timelines). Consult your qualified tax advisor and legal counsel before taking action.

Our Editorial Process:

Our expert team uses AI tools to help organize and structure initial drafts, conduct research, and refine content. Every AI-assisted draft is reviewed, edited, and verified by our human team to ensure accuracy, clarity, and practical value.

By: The Securitas 1031 Insights Team

The Securitas 1031 Insights Team is made up of seasoned, Houston-based legal and tax professionals who specialize in 1031 exchanges and real estate wealth strategy. We work with investors, business owners, and real estate professionals to simplify complex exchange rules and provide clear, actionable guidance. Our content is created for informational purposes and should not replace professional advice. Always consult your CPA, attorney, or qualified intermediary before taking action on a 1031 exchange.