Texas 1031 Exchange Rules: What Houston Investors Need to Know

📌 Key Takeaways

Texas 1031 exchange rules are federal—not state-specific—but Texas closing speed and unusual property types create real risks.

Federal Rules, Texas Execution: The 45-day and 180-day deadlines come from IRS rules, not Texas law—but fast Houston closings can trip you up if your fund routing isn't locked in early.

Real Property Only Now: Since 2017, only real estate qualifies for 1031 exchanges—equipment, furniture, and removable business assets don't count and must be separated from your sale price.

Mineral Rights Can Qualify: Texas classifies severed mineral rights as real property, so oil and gas interests can often be exchanged for other real estate like commercial buildings or land.

Constructive Receipt Kills Exchanges: If sale proceeds hit your bank account—even briefly—your exchange fails instantly, so set up your qualified intermediary before closing, not during.

Water Rights Are Complicated: Perpetual groundwater rights may qualify as real property, but temporary permits and surface water rights usually don't—get documentation reviewed early.

Lock in your exchange structure before closing day, and your tax deferral stays protected.

Houston-area investors holding commercial property, mineral interests, or mixed-asset portfolios will find practical guidance here, preparing them for the detailed timeline and coordination steps that follow.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

The listing is live. Your broker says the buyer wants to close in three weeks. You're planning to defer capital gains through a 1031 exchange—but now you're searching "Texas 1031 exchange rules" because you don't want surprises when closings move this fast in Houston.

The core 1031 exchange rules are federal, not state-specific. Texas matters in practice only when certain property interests must be classified as "real property" and when the closing process needs coordination to avoid constructive receipt. That search leading you toward confusion? The reality is simpler than the results suggest—but the stakes remain real. One misstep in fund handling or property classification can turn tax deferral into an immediate tax bill.

You deserve clarity before you sign closing instructions.

What Houston Investors Mean by "Texas 1031 Rules"

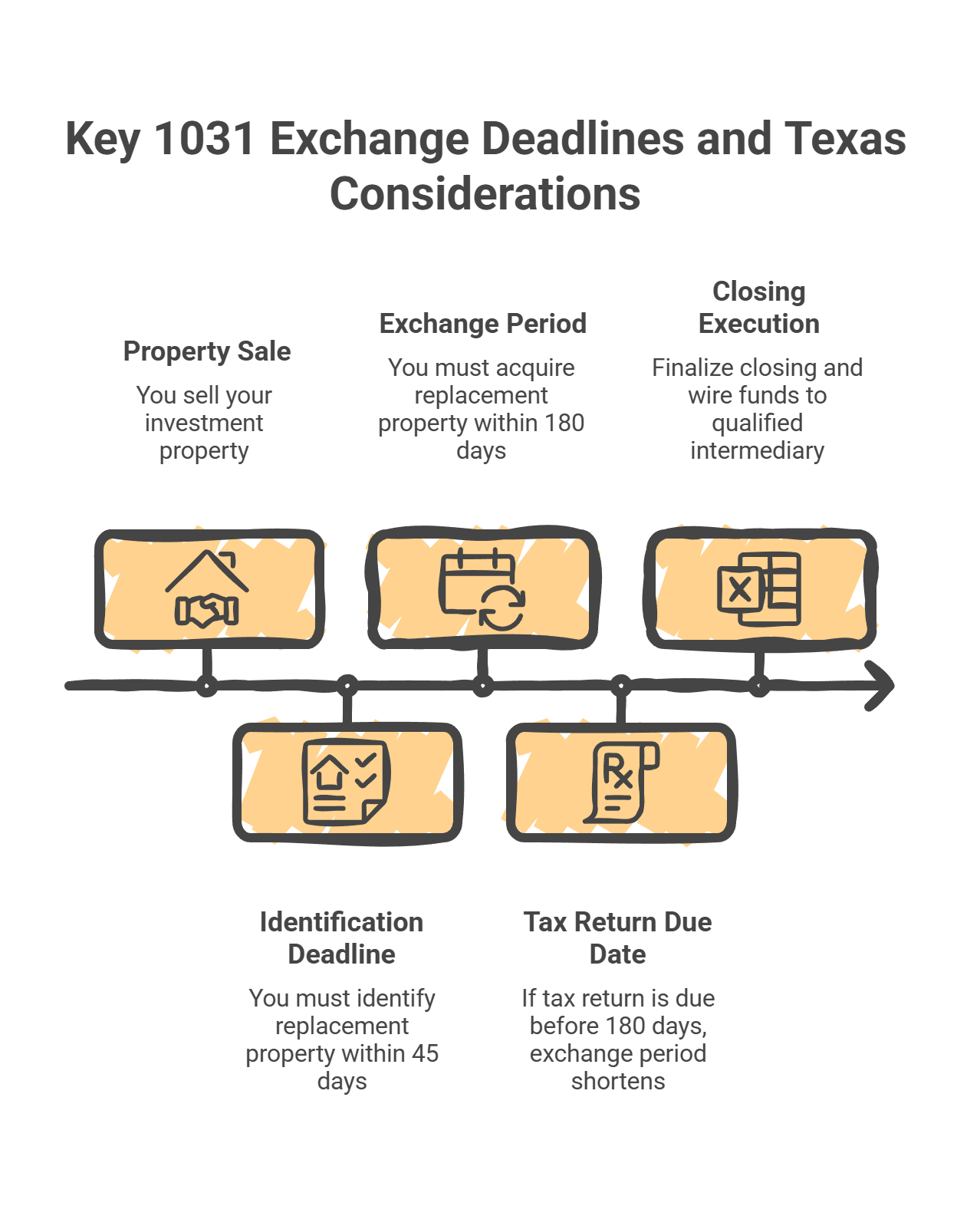

Texas does not set separate 1031 exchange deadlines. Section 1031 of the Internal Revenue Code allows individual real estate investors to defer capital gains taxes when selling investment properties by reinvesting the proceeds into like-kind property. These rules are federal. The 45-day identification deadline and 180-day exchange period are federal mandates under Section 1031. Note that the 180-day period may be shorter if your tax return due date (including extensions) falls before the 180th day.

So where does Texas-specific complexity actually show up?

Two places: property characterization and closing execution.

Property characterization means determining whether what you're selling or buying qualifies as "real property" under the exchange rules. For standard Houston commercial buildings or rental properties, this is straightforward. For mineral interests and water-related rights, Texas state law provides a clear starting point: severed mineral rights and groundwater in place are generally classified as real property interests. However, the 1031 exchange eligibility of water rights hinges on a distinction between perpetual rights and temporary permits. Under Treas. Reg. §1.1031(a)-3 and recent IRS guidance (e.g., PLR 202309007), groundwater rights are typically considered 'like-kind' to fee simple land if they are perpetual in nature and not limited to a specific total volume, whereas surface water—owned by the State of Texas—is usually accessed via permits that may not qualify if they lack sufficient duration or 'real property' characterization under local law. The IRS has issued guidance confirming that state law plays a role in how certain interests are characterized.

Closing execution is where Houston's fast-moving market creates risk. Title companies here move quickly. Wiring instructions get finalized at the last minute. If you haven't locked in your exchange structure before that happens, funds can end up in the wrong hands—literally disqualifying your exchange before it begins.

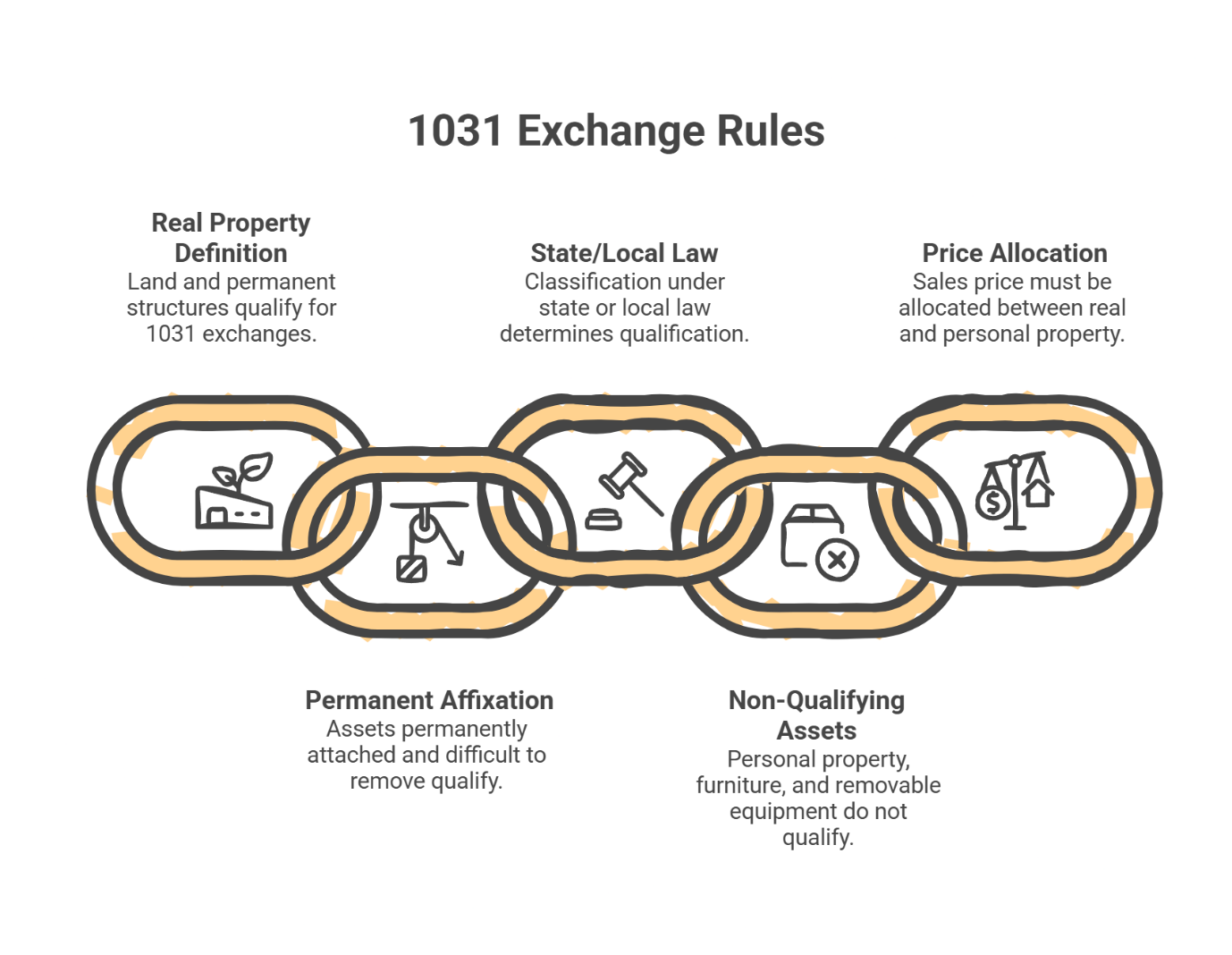

The One Rule Change You Must Know: 1031 Is Real Property Only

Under the Tax Cuts and Jobs Act, Section 1031 now applies only to exchanges of real property. Personal and intangible property no longer qualify. The final Treasury regulations confirmed this limitation, and 26 CFR 1.1031(a)-3 defines what counts as real property for exchange purposes.

This distinction is a primary compliance hurdle for Houston investors holding mixed-asset portfolios.

Real property includes land, permanent improvements, and certain interests tied to land. Machinery or equipment qualifies as real property for exchange purposes only if it is an inherently permanent structure, a structural component, or is classified as real property under state or local law. Crucially, under the final Treasury Regulations (T.D. 9935), the IRS abandoned the 'use test'—meaning a component like a large industrial HVAC system or a specialized walk-in cooler can now qualify as real property if it is permanently affixed, even if it primarily serves a business machinery function rather than the building itself. If an asset is designed to remain in place indefinitely and its removal would cause significant damage, it likely stays within the exchange.

What doesn't qualify? Equipment. Furniture. Removable business assets. That restaurant equipment package bundled into your retail center sale? Personal property—cannot be exchanged tax-free. The heavy machinery in your industrial property? Unless it's permanently affixed and would ordinarily remain for an indefinite period, same problem.

If your Houston property includes both real property and personal property, you'll need to allocate the sales price accordingly. Only the real property portion qualifies for deferral.

For a deeper look at the exchange process and tax savings calculations, visit Securitas 1031's exchange overview.

Texas-Specific Property Types Houston Investors Ask About

Houston sits at the intersection of commercial real estate and energy. That creates property-classification questions you won't encounter in most markets.

Mineral Interests

Texas classifies severed mineral rights as real property, making them potentially eligible for 1031 exchanges. This is significant. If you own mineral rights in Texas—whether attached to surface property or held separately - those rights are generally classified as real property and can be exchanged for other real property, such as fee simple land or commercial buildings.

In Texas, oil rights can be real estate.

The key requirement: the interest must be structured as real property under both state law and IRS guidelines. Perpetual mineral rights and standard royalty interests generally qualify. Short-term production payments or limited-quantity extraction rights may not. A Texas county government FAQ on mineral interests provides additional context on how these interests are treated locally.

If your Houston-area property includes mineral interests, get your documentation reviewed before you identify replacement property. For a screening approach tailored to Texas investors, use this like-kind property checklist.

Water-Related Interests

Water rights in Texas represent significant complexity. Under Texas law, groundwater and surface water rights are distinct; while certain perpetual rights or shares in a mutual ditch company may qualify as real property, temporary permits or contract-based rights generally do not.

Leasehold and Development Rights

Long-term leaseholds (typically 30 years or more remaining) generally qualify as real property for exchange purposes. Development rights tied to land may also qualify, depending on their structure.

The questions to ask: What exactly is being transferred—fee simple ownership, a long-term leasehold interest, or a defined right tied to land use? Is the interest recorded, assignable, and conveyed through standard closing instruments? Does the purchase and sale agreement clearly describe the interest, and do closing instructions match that description?

If the answer to any of these is unclear, start gathering paperwork now—not during your identification period.

Deadlines Still Win: Your 45-Day and 180-Day Planning Checklist

The federal deadlines don't flex for weekends, holidays, or Houston closing schedules.

Before You List:

Decide whether you want exchange treatment

Identify two or three potential replacement property types

Contact a qualified intermediary to set up your exchange account

After You Sign a Purchase Contract:

Confirm your QI is documented as the fund recipient in closing instructions

Lock in your closing date with enough buffer to avoid deadline collisions

Begin active replacement property identification

Your 45-day identification period includes every calendar day—weekends, holidays, all of it. Unlike most IRS deadlines, 1031 deadlines are not extended to the next business day if they fall on a Saturday, Sunday, or legal holiday.

Identification pressure drops significantly when candidate replacement properties are already being evaluated before closing. For guidance on what happens if you miss the 45-day deadline—and how to prevent it—review the IRS requirements carefully.

Houston Closing Reality: Title Companies Move Fast

The theoretical risk everyone warns about—constructive receipt—usually isn't a theoretical problem. It's an execution breakdown.

Constructive receipt occurs when the property owner has the ability to control the sale proceeds, such as when funds land in your bank account or an escrow account you can access. Here's how it happens in Houston: Closing gets scheduled quickly. The title company prepares standard wire instructions. Funds get routed to your bank account—or to an escrow account you can access—instead of to your qualified intermediary. The exchange fails before you even realize there's a problem.

If you receive any money—a wire to your bank account or even an uncashed check with closing proceeds—that capital becomes irreversibly taxable.

The solution is structural, not attentive. Your exchange needs to be set up before closing so the fund-handling path is defined and documented.

Who Does What in Your Exchange:

You (the exchanger): Confirm exchange intent, sign exchange documents, approve the identification plan, and make acquisition decisions.

Your broker: Manage timing expectations, communicate exchange intent to all parties, and help surface replacement opportunities early.

Title company: Follow written instructions for disbursement and execute closing documents with correct fund routing to the QI.

Your CPA: Advise on tax implications, support allocation questions, and handle reporting considerations.

Qualified intermediary: Coordinate exchange documentation, hold funds to prevent constructive receipt, and transfer funds for the replacement purchase.

Coordination between these parties prevents most exchange failures. The problems occur when one party doesn't know an exchange is happening—or when instructions change at the last minute without the QI in the loop.

A Simple Pre-Closing Readiness Check

Before you sign final closing instructions, answer these questions:

Standard Sale + Standard Replacement = Simpler Path

Is your property a straightforward commercial or residential investment you own directly?

Is your replacement target also standard real estate with conventional title and clean documentation?

Are you working with a QI who will hold funds?

If yes to all three, your exchange path is relatively clear. Execute the structure, meet the deadlines, complete the acquisition.

Any Non-Standard Element = Start Earlier

Does your property include mineral interests, unusual leaseholds, or water rights?

Is any part of the sales price allocated to personal property?

Are you considering a reverse exchange or construction exchange?

Are there complex title issues or ambiguous property descriptions?

If yes to any of these, start the planning process earlier. Get documentation reviewed. Confirm property characterization before you're under deadline pressure.

The difference between a successful exchange and a failed one usually isn't knowledge—it's timing. Property owners who set up the structure before closing protect their equity. Those who scramble after signing create risk.

For individual investors and families focused on preserving wealth across generations, a properly executed 1031 exchange keeps more capital working in your personal real estate holdings rather than going to taxes.

Ready to talk through your specific situation? Schedule a free consultation with Securitas 1031's attorney-led team in Houston. If you're already under contract and need to move quickly, call 713-275-8112.

Securitas 1031, LLC 440 Louisiana St, Suite 1100, Houston, TX 77002 Tel: 713-275-8112

Disclaimer: This article provides general information for educational purposes and is not legal or tax advice. Individual outcomes depend on factors such as your property type and ownership structure, how your closing is executed, whether any non-standard property interests are involved, and whether exchange funds are handled to avoid constructive receipt. For guidance tailored to your specific transaction and timeline, consult a qualified professional.

Our Editorial Process:

Securitas 1031 content is developed using primary IRS guidance, Treasury regulations, and internal exchange procedures to explain technical topics in clear, practical language. We review drafts for terminology consistency and deadline accuracy, and we update published content when rules, guidance, or common transaction practices change. For transaction-specific guidance, schedule a consultation with our team.

By: The Securitas 1031 Insights Team.

Securitas 1031 is a Houston-based, attorney-led qualified intermediary that structures standard, reverse, and improvement 1031 exchanges for direct property owners, with a focus on secure handling of exchange funds and disciplined compliance workflows.