Why Your Title Company’s Affiliate QI Puts Your Exchange at Risk

📌 Key Takeaways

Your title company's "convenient" QI referral may prioritize closing speed over the compliance controls that protect your tax deferral.

Separate Closing from Compliance: Your title company closes deals; your QI guards your money—mixing these roles under one roof creates conflicts when deadlines pressure both.

Verify Fund Protection: Demand a segregated account with your name on it, not pooled funds that could vanish in a bankruptcy like LandAmerica's $420 million collapse.

Ask About Complex Deals: If you might buy before you sell or need construction draws, confirm your QI has the structure and staff for reverse and improvement exchanges.

Decide Before Closing Day: Engage your QI while still under contract so you have time to review agreements and confirm controls—not at the closing table under pressure.

Grill the Referral: Ask who authorizes wires, what happens when closing and documentation timelines conflict, and whether attorney oversight is real or just marketing.

Convenience isn't compliance—vet controls before you sign.

Real estate investors evaluating 1031 exchange providers will find a clear framework for protecting their equity, preparing them for the detailed due diligence checklist that follows.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

The closing table. The title officer leans in and says, "We can handle the exchange too—just use our affiliate QI."

It sounds simple. One less vendor. One fewer relationship to manage. Your closing is tight, and adding complexity feels unnecessary.

But a 1031 exchange is not a closing function. It is a compliance process where one misstep can trigger a tax bill that wipes out years of equity growth. Before you sign anything, you need a clear framework to decide whether that "convenient" referral actually protects your deal—or puts it at risk.

The Convenience Risk: Why Your Closing Agent Isn't Your QI

Your title company is paid to close transactions. They verify ownership, clear liens, issue title insurance, and make sure everyone walks away with the right documents signed. That work is essential.

Your qualified intermediary has a completely different job. A QI must hold your exchange proceeds under a written agreement that prevents you from touching the funds until they are used to purchase your replacement property. They also structure the documentation so the IRS recognizes the transaction as an exchange rather than a taxable sale.

Bundling these functions under one corporate umbrella feels efficient. But efficiency and compliance are not the same thing. When your closing agent and your exchange-funds holder share the same parent company, the lines between "completing your closing" and "protecting your exchange" can blur—especially under pressure.

In Houston, deal velocity makes this worse. A same-week closing leaves little room to audit processes or pivot providers once wiring instructions are already being circulated.

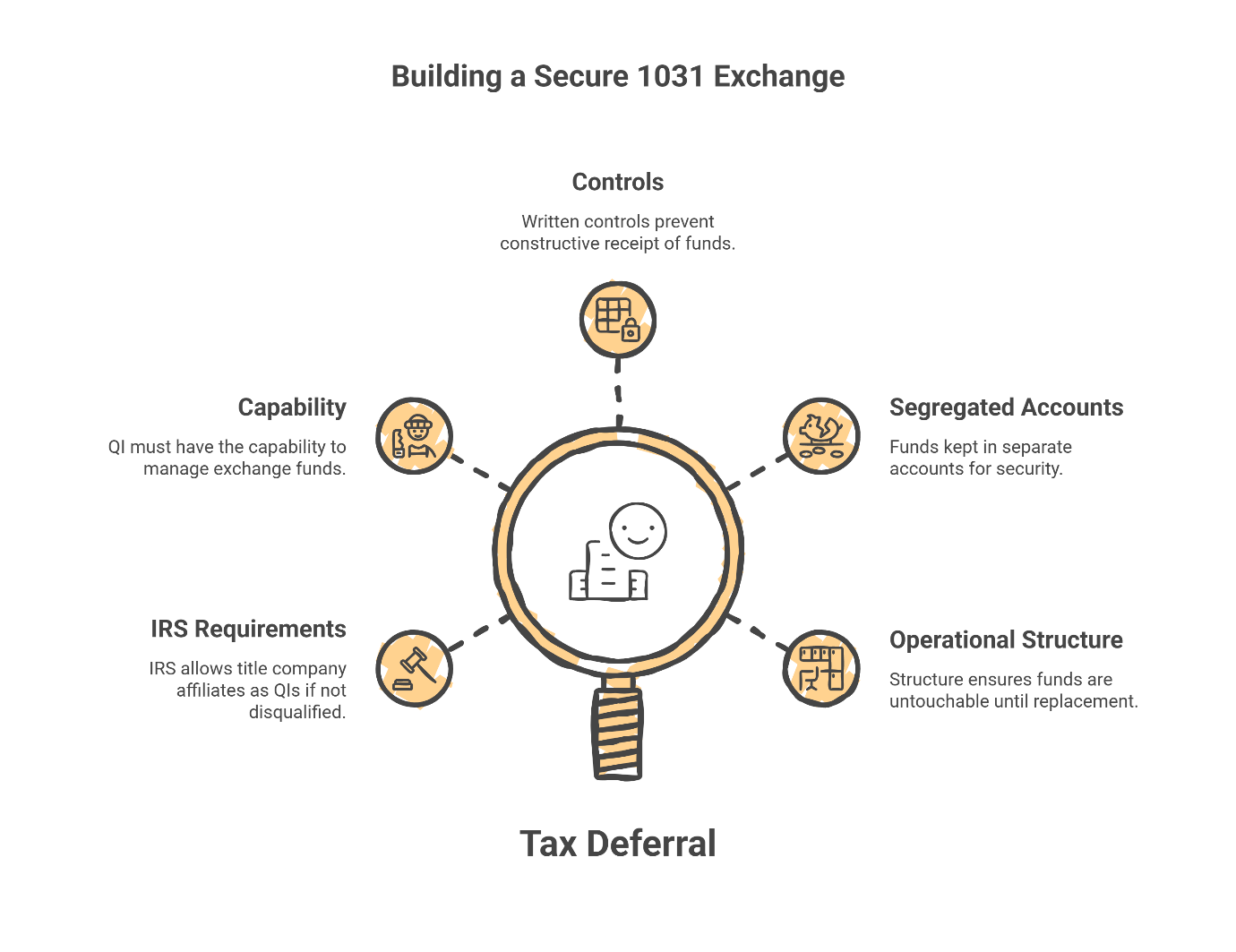

What the IRS Requires (and What It Doesn't)

The IRS does not prohibit you from using a title company's affiliate as your QI. A title company can serve as a qualified intermediary in a Section 1031 like-kind exchange, provided the relationship does not automatically make it a "disqualified person."

The issue is not permission. The issue is capability and controls. The affiliate relationship is not the only factor that matters—capability and controls matter more than branding.

To defer capital gain tax liability with a 1031 exchange, the taxpayer must never be in constructive receipt of the proceeds from the sale. Constructive receipt means you have the ability to access, control, or benefit from the funds—even if you never actually touch them. A taxpayer is in constructive receipt of money or property at any time the money or property is credited to the taxpayer's account, set apart for the taxpayer, or otherwise made available so that the taxpayer may draw upon it at any time.

Your QI's job is to eliminate that risk. That requires written controls, segregated accounts, and an operational structure that keeps your funds untouchable until they are wired to purchase your replacement property. For the foundational framework, review 26 CFR §1.1031(k)-1 and the IRS overview on like-kind exchanges.

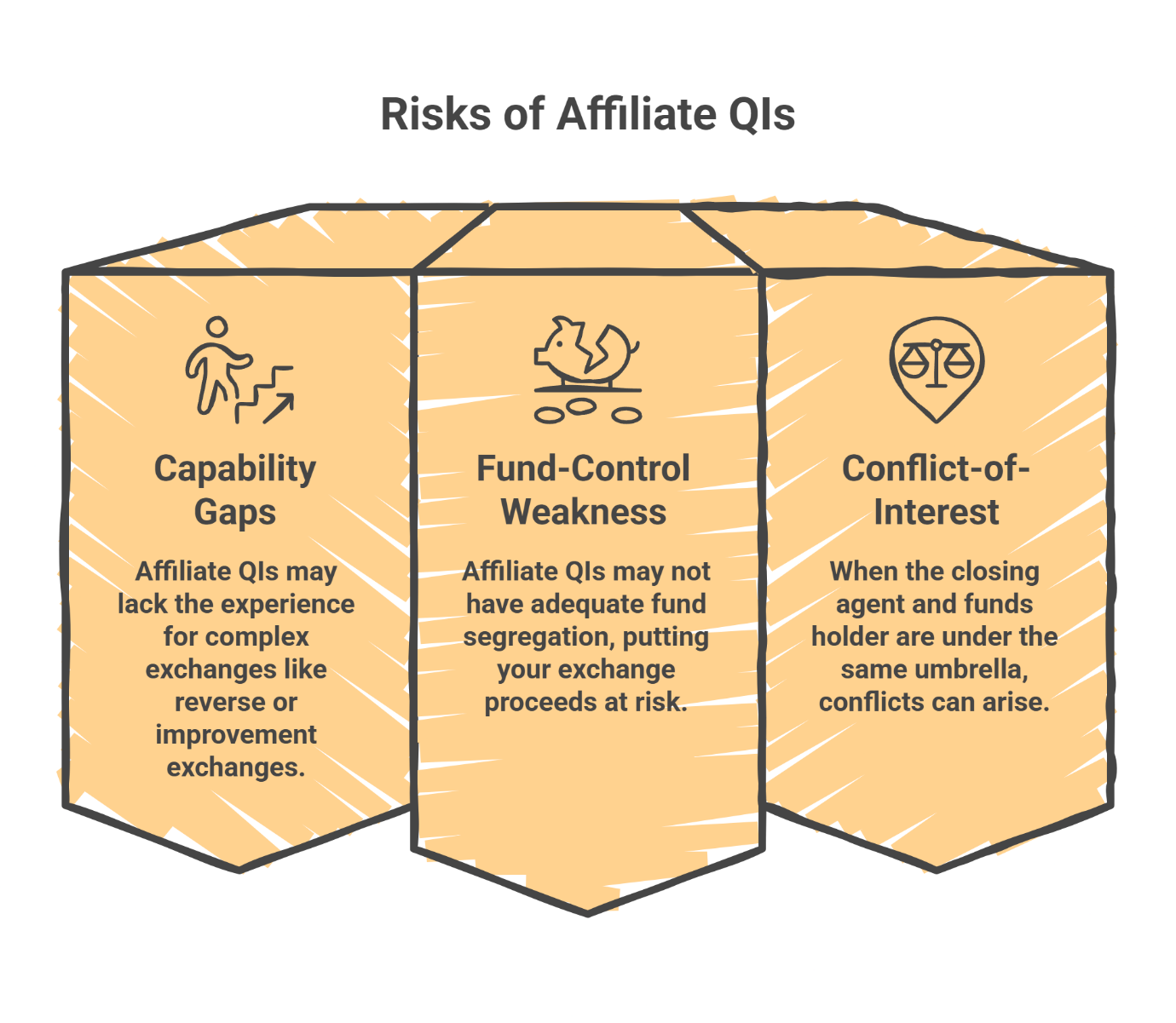

3 Ways an Affiliate QI Can Put Your Exchange at Risk

1. Capability Gaps for Reverse and Improvement Exchanges

If your deal might require you to acquire the replacement property before you sell your current asset, you need a QI who can operate as an Exchange Accommodation Titleholder. An EAT acquires and holds the target property in a separate special purpose entity, typically a single-member LLC. This 'parking' arrangement generally follows the safe harbor guidelines established under Revenue Procedure 2000-37, which permits an Exchange Accommodation Titleholder (EAT) to hold property for up to 180 days

Not every QI has the legal structure, staffing, or experience to handle these transactions. A QI who routinely processes standard forward exchanges may not have a standing process for EAT structures. Ask directly.

2. Fund-Control Weakness

In 2008, LandAmerica 1031 Exchange Services filed for bankruptcy while holding approximately $420 million in exchange proceeds. While the majority of the 450 impacted investors held funds in commingled accounts, a smaller group had requested 'segregated' sub-accounts. However, in the landmark case Millard Refrigerated Services v. LandAmerica 1031 Exchange Services, the bankruptcy court ruled that even these segregated funds were property of the bankruptcy estate because the exchange agreements lacked specific 'express trust' language. The lesson is clear: segregation alone is not enough; you must demand a true Qualified Trust or Escrow Agreement aimed at shielding assets from bankruptcy creditors.

The lesson is clear: demand fund segregation. Your exchange proceeds should sit in a separate, clearly titled account—not commingled with other client funds or corporate assets. Ask who can authorize wires, what documentation controls exist, and whether the QI maintains fidelity bonding or errors-and-omissions insurance.

3. Conflict-of-Interest and Priority Risk

When the closing agent and the funds holder sit under the same corporate umbrella, a structural tension can arise. The title company's primary goal is completing the closing. If pressure mounts—same-day changes, wire timing conflicts, last-minute requests—whose priority governs?

The safest posture is to treat this issue as verification, not accusation. Verify who controls the funds. Verify how wires are authorized. Verify what happens when a same-day change is requested. These questions deserve answers before you sign: What happens if the title officer is pushing a same-day change, but the QI documentation isn't ready? Who has final authority over fund disbursement?

"Convenience isn't compliance. When the entity prioritizing the closing date also controls the compliance breaks, your tax deferral becomes the casualty of speed."

Due Diligence Checklist: What to Ask Before You Sign

Before accepting any QI referral, run through these questions:

Reverse/improvement readiness: "If my deal turns into a reverse or improvement exchange, do you have a standing process for EAT structures?"

Fund segregation: "Are my exchange proceeds held in a segregated account with my name on it—or are funds commingled?"

Wire authorization: "Who can authorize wires from my exchange account, and what is the approval process?"

Documentation discipline: "Is there a written description of fund controls, and do you maintain an audit trail process?"

Same-day pressure: "What happens if the title officer needs to close today, but the exchange documentation isn't finalized? Who decides?"

Attorney oversight: "Do you provide attorney oversight for exchange documentation review? If yes, what does that mean operationally?"

For a deeper dive on vetting QI fund controls, see How to Choose a Qualified Intermediary: 5 Security Questions to Ask.

A Safer Decision Framework: Decouple Closing Agent from QI

The safest approach is to decide your QI before your relinquished property closes—not at the closing table.

Step 1: Select and engage your QI while you are still under contract on the sale. This gives you time to review the exchange agreement, confirm fund controls, and verify capability for your specific deal structure.

Step 2: Ask for written wiring and hold procedures upfront. A reputable QI should be able to provide a one-page fund controls summary before you sign anything.

Step 3: If you decide to switch QIs, coordinate with the title company early. Do not wait until the day of closing. A last-minute change creates exactly the kind of pressure that leads to common 1031 mistakes that trigger a tax bill.

If your deal might require a reverse structure, improvement draws, or any complexity beyond a standard forward exchange, flag it now. For background on why the DIY approach puts your equity at risk, start there.

If referral pressure is part of the experience, additional context is available in The Broker's Liability Guide to 1031 Referrals.

If a Reverse or Improvement Exchange Might Be Needed, Decide Now

Complex deal structures cannot survive a deadline-day handoff. A practical way to flag the need early:

Buying first: You need to close on a replacement before selling your current property.

Planning significant work: The replacement property requires construction or major improvements.

Expecting multiple draws: Contractor payments and construction draws will need coordination during the exchange period.

When any of these factors are present, the QI decision should be made as early as the acquisition strategy—not after the title company has already drafted closing documents.

Frequently Asked Questions

Is it allowed to use my title company's affiliate as the QI?

Yes, it can be allowed. The IRS does not prohibit affiliate relationships outright. But "allowed" is not the same as "protected." Vet the QI's capabilities, fund controls, and conflict-of-interest safeguards before signing. See IRS guidance on like-kind exchanges for additional context.

When do I need to engage a QI?

Before your relinquished property closes. The 1031 exchange must be established and in place at or before the closing of the first property in the exchange. Once the sale has closed, it is too late to start an exchange.

What is constructive receipt in plain English?

Constructive receipt means you had the ability to access or control the exchange funds, even if you never actually touched them. If the IRS determines you had constructive receipt, your exchange fails and you owe taxes on the gain.

How do reverse exchanges "park" property?

Using an Exchange Accommodation Titleholder, the title to the replacement property is held for up to 180 days, allowing the taxpayer to transfer the relinquished property to a buyer. The EAT holds the property until your sale closes, then transfers it to you to complete the exchange.

What documents should I expect from a QI?

Documents vary by deal, but commonly include exchange agreements, assignment documents, notices to parties involved, and written procedures for holding and disbursing exchange proceeds.

Take Action Before the Closing Table

The closing agent drives the timeline; the Qualified Intermediary guards the safe harbor. When those functions blur, your exchange is at risk.

Decide your QI before the sale closes. Ask the hard questions about capability, fund controls, and conflict safeguards. And if a referral feels rushed, it probably is.

Learn more about 1031 exchanges to build a stronger foundation before your next deal.

Ready to discuss your specific situation?

Schedule a Free Personal Consultation with the Securitas 1031 team. Our attorney-led approach ensures your exchange receives the individual attention and compliance expertise it deserves.

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. Every exchange is fact-specific. Consult your tax advisor and legal counsel regarding your situation.

By: Securitas 1031 Insights Team

Securitas 1031—named for the Roman goddess of security and stability—is led by Charles H. Mansour, a tax attorney with over 30 years of experience, 18,000+ closings, and $3 billion in transactions. Our team of attorneys and real estate professionals provides individual property owners with secure, compliant 1031 exchange services and the personal attention every exchanger deserves.