The 45-Day Identification Rule: A Strict Checklist for Developers

📌 Key Takeaways

Missing the 45-day deadline to name your replacement properties kills your entire 1031 exchange—no exceptions, no extensions.

Start Before Day Zero: Build your property target list before your sale closes, because the 45-day clock starts whether you're ready or not.

Get Specific on Paper: Vague descriptions like "the corner lot" won't count—you need exact addresses, legal descriptions, and parcel numbers in a signed document.

Pick Your Rule Early: Choose between the 3-property, 200%, or 95% identification method by Day 30 so your team can verify your choices work with lenders and title.

Deliver With Proof: Send your signed identification letter to your Qualified Intermediary with tracking and get written confirmation before midnight on Day 45.

Name Backup Properties: If your first-choice deal falls through after Day 45, you can't add new properties—so identify realistic alternatives from the start.

Treat Day 45 like a closing deadline, because that's exactly what it is.

Property owners planning a 1031 exchange will find a clear roadmap here, preparing them for the detailed timeline and checklist that follows.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

It's 4:47 PM on Day 44.

You have targets in mind. Your lender has favorites. Your title company has working assumptions. But nobody has a signed identification document with unambiguous property descriptions delivered to the right party. The clock runs out at midnight tomorrow.

This is how exchanges fail in the real world—not from lack of intent, but from paperwork timing. For property owners running reverse exchanges, construction deals, or acquiring multiple replacement properties, the 45-day identification deadline isn't a suggestion. It's a hard stop that includes weekends and holidays, offers no extensions, and can turn a carefully planned reinvestment into an immediate tax problem.

The good news: this is entirely preventable. What follows is the operational checklist that keeps your exchange on track from Day 0 through Day 45.

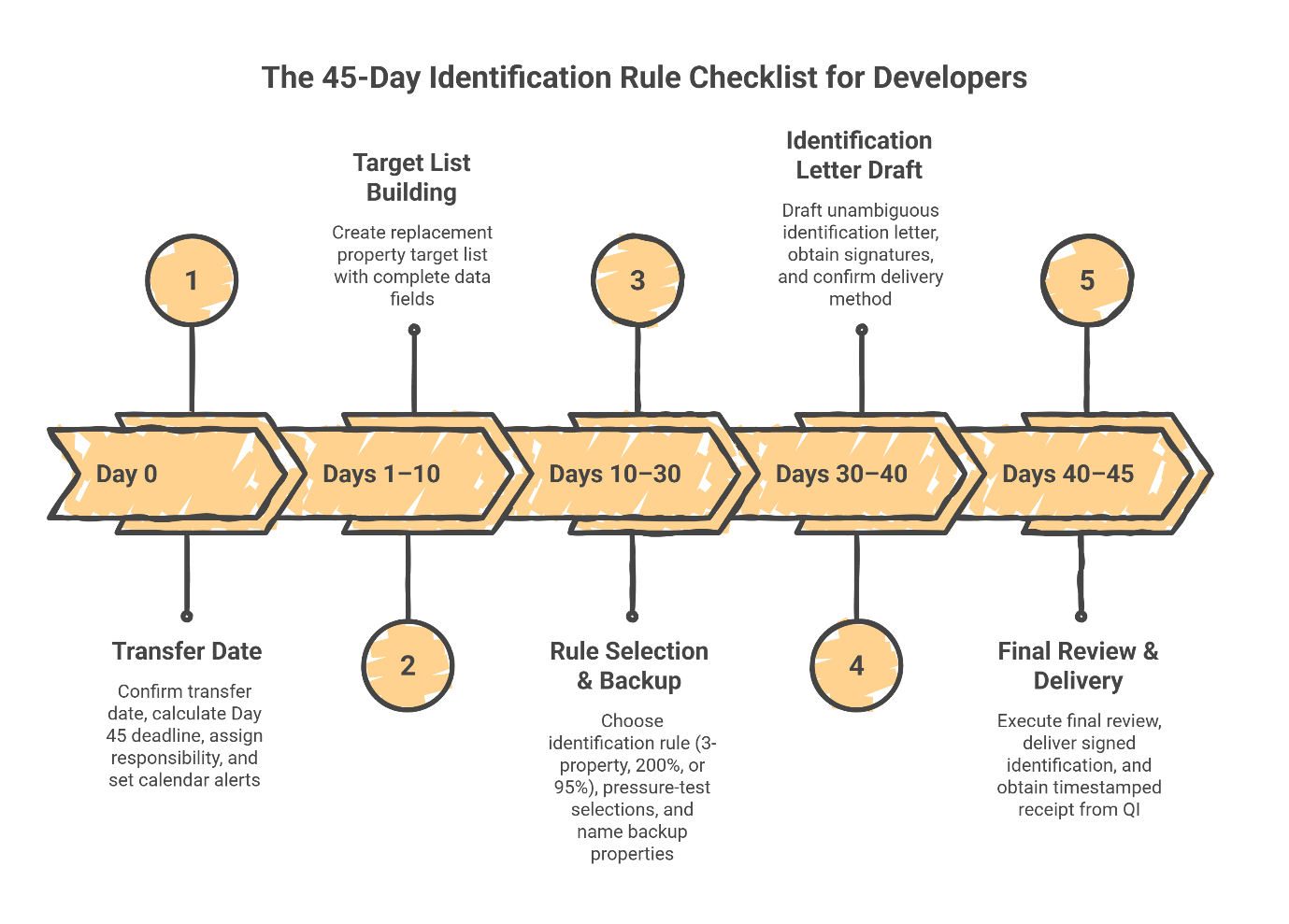

The Day 0 to Day 45 Checklist

Your 45-day identification period begins on the transfer date of your relinquished property—not the listing date, not the contract date. According to Treasury Regulation §1.1031(k)-1, the period ends at midnight of the 45th calendar day.

Here's your operational sequence:

Day 0 (Transfer Date): Confirm the exact transfer date and calculate your Day 45 deadline. Designate one person responsible for the identification process—whether that's you, your CPA, or your attorney. Set calendar alerts for Days 10, 30, 40, and 44.

Days 1–10: Build your replacement property target list with complete data fields—street address or legal description, seller name, and parcel identifiers for each candidate.

Days 10–30: Select which identification rule you'll use (3-property, 200%, or 95%). Pressure-test your selections against underwriting timelines and lender requirements. Name backup properties.

Days 30–40: Draft your Identification Letter. Verify every property description is unambiguous. Obtain required signatures. Confirm delivery method and recipient.

Days 40–45 (Final Window): Execute final review. Deliver the signed identification to the proper party. Under Treasury Regulations, the identification must be 'sent' before the end of the identification period; however, for audit protection, you should ensure the document is transmitted and obtain a timestamped receipt confirmation from your Qualified Intermediary (QI) before midnight on Day 45. (Treas. Reg. §1.1031(k)-1(b)(2)).

"Day 45 is final. Treat it like a closing deadline—because it is."

The 45-Day Countdown Calendar

A countdown calendar makes the deadline visible and keeps you and your advisors aligned. Here's how to structure it:

Milestone alerts:

Day 10: Target list must be "identification-ready" with unambiguous descriptions for each candidate.

Day 30: Rule selection finalized; backups named and validated against lender and title requirements.

Day 40: Letter drafted, descriptions verified, signatures staged.

Days 40–45: Final window—delivery and receipt confirmation focus only.

How to use this calendar:

Designate one person responsible on Day 0 and add the calendar to a shared workspace with your CPA, attorney, and broker. Set automated reminders at Day 10, Day 30, Day 40, and Day 44 morning. Reserve Days 40–45 for verification and delivery controls. Store evidence (signed letter, proof of delivery, and confirmation) in a single file for your records.

Days 1–10: Build Your Replacement Target List the Right Way

A solid target list is not a spreadsheet of ideas. It's a pre-identification package that can be converted into a compliant written identification without scrambling on Day 44.

Minimum fields to capture for each candidate:

Street address and/or legal description

Parcel or APN identifiers where applicable

Seller/owner name as currently titled

Property type and intended use (for your own planning)

Plan A / Plan B / Plan C designation to keep your priorities clear

Notes if you're acquiring multiple properties or planning improvements

For property owners acquiring multiple replacement properties:

If you're exchanging into several properties—whether assembling adjacent parcels, separating land from improvements, or acquiring a mix of property types—keep separate notes for each. This is common for individual investors and family-owned entities looking to diversify or reposition their holdings through direct ownership.

By Day 10, you should be able to answer one question: "Can each target be identified unambiguously, in writing, without guessing?" If the answer is no, the list isn't ready.

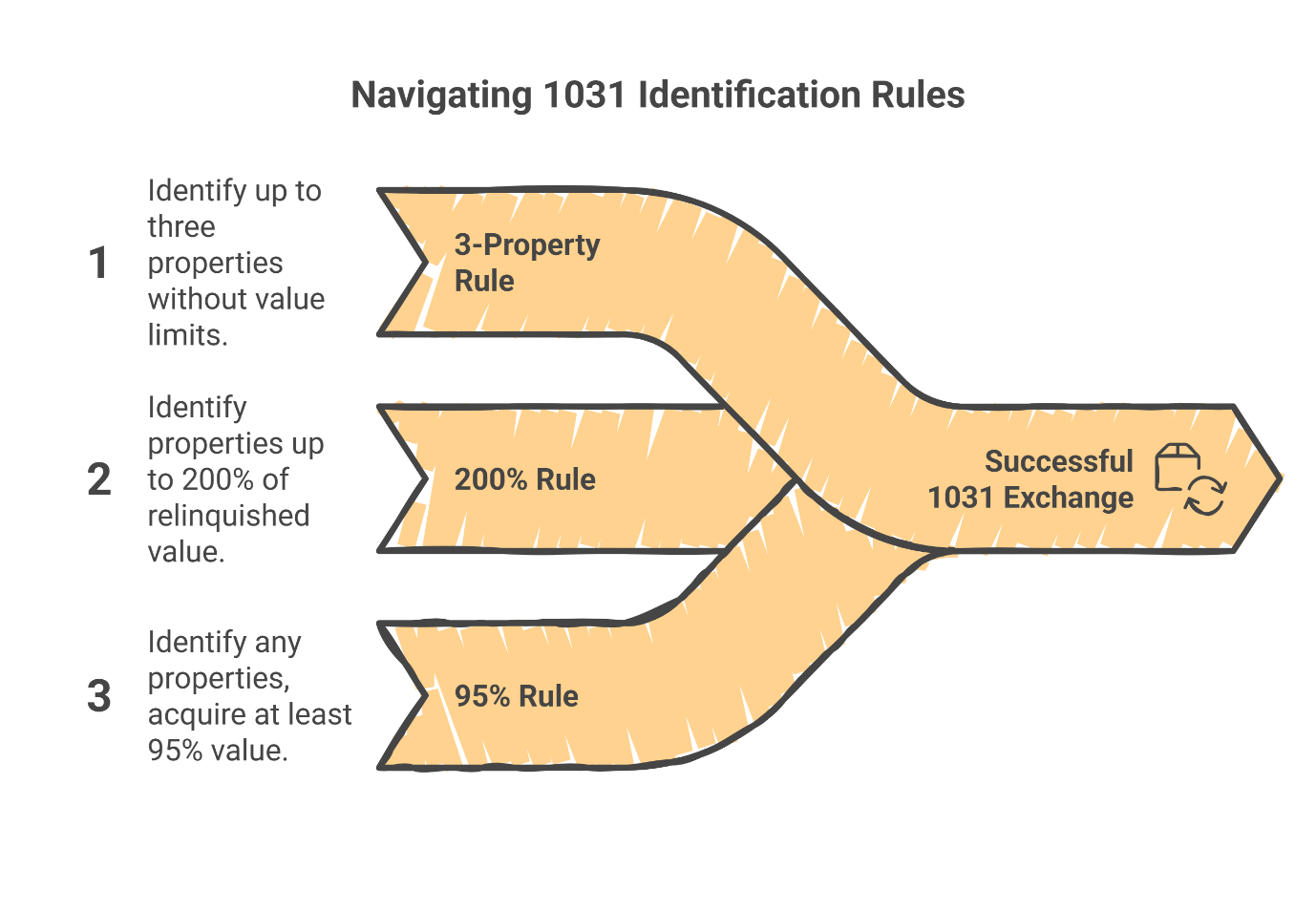

The Three Valid Identification Methods

The IRS provides three rules for identifying replacement properties. Each has specific requirements, and you must stay within the boundaries of whichever rule you choose. Per Treasury Regulation §1.1031(k)-1(c), your identification must be in a signed, written document delivered to the proper party within the 45-day window. For additional context, see the IRS like-kind exchanges real estate tax tips.

1. The 3-Property Rule

You can identify up to three properties regardless of their total fair market value. This rule works best when you have two or three high-confidence targets and don't need additional flexibility. The trade-off: fewer backups mean higher dependency on a short list.

2. The 200% Rule

You can identify more than three properties, but their combined fair market value cannot exceed 200% of the relinquished property's value. This rule works best when you're evaluating multiple options or acquiring several smaller properties. The trade-off: you must maintain value discipline to avoid accidentally exceeding the threshold.

3. The 95% Rule

You can identify any number of properties at any value, but you must actually acquire at least 95% of the aggregate value of everything you identified. This rule works best only when you have near-certainty on closing every target. The trade-off: low tolerance for failed acquisitions makes this the highest-risk option.

For most individual investors working with a 1031 exchange qualified intermediary, the 3-property or 200% rule provides sufficient flexibility without the compliance exposure of the 95% rule. For a deeper breakdown of each method, see the 45-day identification rules explained.

Identification Letter Workflow

Your identification isn't valid until it exists as a signed, written document delivered to the correct party. While a standard text-based email thread typically fails to meet the IRS signature requirement, a digital document (such as a PDF) that is electronically signed via a compliant platform (e.g., DocuSign) or a scanned copy of a wet-ink signature sent via email is legally sufficient. A verbal agreement, however, never satisfies the regulatory standard. (Treas. Reg. §1.1031(k)-1(b)(2); ESIGN Act of 2000). A verbal agreement doesn't count. Here's the workflow:

What the document must contain:

Your name and taxpayer identification

The relinquished property transferred

Each replacement property identified with unambiguous descriptions (street address and/or legal description)

Which identification rule you're using

Your signature and date

Who receives it:

The identification must be delivered to a party involved in the exchange who is not a disqualified person—typically your Qualified Intermediary. Confirm the required recipient before drafting.

How to build a confirmation trail:

Send via a method that provides delivery confirmation (certified mail, overnight courier with tracking, or secure electronic delivery with read receipt). Retain timestamped proof of delivery. Obtain written acknowledgment of receipt from your QI.

Template structure (fill in your specifics):

IDENTIFICATION OF REPLACEMENT PROPERTY

Date: [Date]

Exchanger: [Your Name/Entity]

Relinquished Property: [Address/Legal Description]

Identification Rule: [3-Property / 200% / 95%]

Replacement Properties Identified:

[Full Address and/or Legal Description]

[Full Address and/or Legal Description]

[Full Address and/or Legal Description]

Signature: ____________________

Date: ____________________

Days 40–45: The Final Window Protocol

Final-week failures are usually procedural, not technical. A clean protocol prevents "almost compliant" mistakes.

Verification steps before delivery:

Document integrity check: Property descriptions are specific, consistent, and match what title and lender are underwriting.

Signature check: You (or your authorized representative) executed the identification document and dates are accurate.

Delivery proof check: Delivery method is trackable and recipient confirmation is staged.

Fallback move: If a target falls through, immediately pivot to a backup that fits the chosen rule. Do not rely on informal email chains.

Common Failure Points and How to Prevent Them

"I had a list in email."

Fix: A signed, written identification document delivered to the proper party is required. Email discussions don't satisfy the regulatory requirement. Draft the formal letter and get signatures.

"I identified 'a parcel' without specifics."

Fix: Use unambiguous descriptions. "The northwest corner lot" isn't sufficient. Include the full street address, legal description, or parcel number so there's no question which property you mean.

"I waited until after closing to start."

Fix: Begin your target list development before your relinquished property closes. Assign responsibility at contract signing, not transfer. The 45-day clock starts whether you're ready or not.

"My broker, lender, and title company weren't aligned."

Fix: Share your identification target list with all parties before Day 30. Misalignment between your plans and your lender's requirements is a common source of last-minute scrambles.

If you're unsure what happens if you miss the 45-day deadline, the short answer is: the exchange fails. While there is generally no grace period or extension, limited exceptions exist for taxpayers in federally declared disaster areas or those serving in combat zones (Rev. Proc. 2018-58). The equity you planned to defer becomes taxable.

Reliable Compliance: Systematizing Your 45-Day Window

For property owners running complex exchanges—reverse structures, construction or improvement builds, or multiple replacement property acquisitions—the 45-day identification requirement is just one piece of a larger compliance framework. The difference between a successful exchange and a failed one often comes down to documentation discipline, timeline enforcement, and a confirmation trail that holds up to scrutiny.

Securitas 1031 works with individual investors, business owners, and families in the Houston area to build Day-45 systems before the clock starts. Our attorney-led team specializes in the compliance-intensive exchanges that direct property owners typically run—where the stakes are higher and the margin for error is smaller.

If you're preparing to sell a property and want a strategic 1031 exchange timeline built around your acquisition targets, schedule a consultation before closing. The best time to set up your identification workflow is before Day 0—not Day 44.

Disclaimer: This content is for informational purposes only and does not constitute legal, tax, or financial advice. 1031 exchange rules are highly technical and outcomes depend on your specific facts (including property descriptions, identification method, delivery/receipt process, and transaction timelines). Consult your qualified tax advisor and legal counsel before taking action.

Our Editorial Process:

Our expert team uses AI tools to help organize and structure initial drafts, conduct research, and refine content. Every AI-assisted draft is reviewed, edited, and verified by our human team to ensure accuracy, clarity, and practical value.

By: The Securitas 1031 Insights Team

The Securitas 1031 Insights Team is made up of seasoned, Houston-based legal and tax professionals who specialize in 1031 exchanges and real estate wealth strategy. We work with investors, business owners, and real estate professionals to simplify complex exchange rules and provide clear, actionable guidance. Our content is created for informational purposes and should not replace professional advice. Always consult your CPA, attorney, or qualified intermediary before taking action on a 1031 exchange.